Selling volatility (vol) in markets was a solid trade last week, but for those trading instruments outside of the options space, the weekly implied moves (derived from options pricing) served as another good risk guide for spot FX traders. Offering good insights as to the extent of the moves in price on the week.

This week we see that vols are still incredibly low, with many pairs below the 10th percentile of the 12-month range. The EUR stands out as the mover on the week, but even then we're defined (in EURUSD) by a 1.1404 to 1.1202 range, where traders will be willing sellers into 1.1430 (R3) in my view. USDJPY implied vol is shot to pieces, and the market expects a 64-pip move on the week, where we can see on the higher timeframes strong bids coming into the market below 106.50 since 11 June - so unless we see equity vols really come alive, which seems unlikely but not out of the question given the start of US2Q earnings season, I'd be expecting clientsto put buy orders into here.

What key event risks catch my eye this week?

Firstly, we've seen a modest breakdown in the correlation between the S&P500 and the USD, but it's still elevated and I would therefore still have the US500 on the radar. If we see price kick on through 3191, which is playing out so far on the futures re-open today thenrisk FX and high carry currencies will be favoured - US Q2 earnings season kicks off this week for US Share CFD traderswith JPM starting proceedings tomorrow before the S&P500 cash open. Conversely, a close through 3130 brings us back to the 200-day MA and this should see a better bid in the JPY and CHF.

As I focus on quite intently in the 'Daily Fix', US real Treasury yields remain key to markets - they are the common denominator between gold and growth equity moves. If real yields head lower then my thesis remains to buy the NAS100, and gold and favour short USD positions. Obviously, if yields rise then that trade reverses and it is certainly a crowded one, with USD shorts increasing last week.

Fed speakers due this week

The Fed chatter fest will be in play, with my focus being on Lael Brainard's discussion on economics and policy. Two consideration I have is whether certain Fed officials increase their tone of concerns around the COVID19 dynamics that are well documented in a number of US states. And, whether the Fed starts to talk about froth (code for excessive speculation) appearing in parts of the capital markets - this seems unlikely, but it is not out of the realms of possibility.

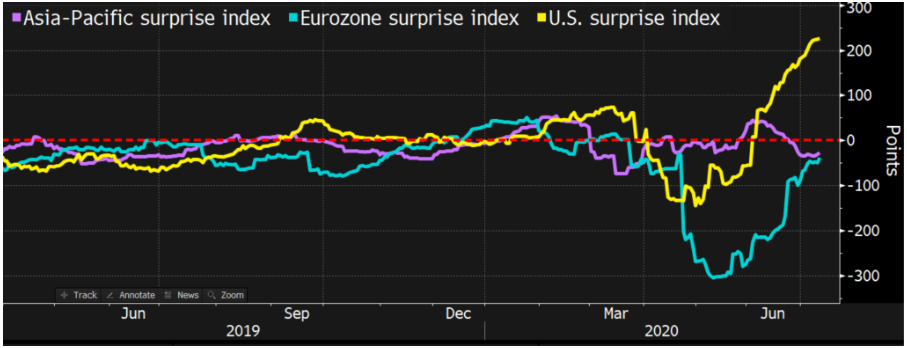

Citigroup economic surprise index - US and EZ data in particular has been beating consensus expectations on a consistent basis of late. Will that mean that better data fails to inspire?

Tuesday

China - June trade data (exports/Imports) - An important data point, but given there is no set time, and forecasting is a lottery, it rarely proves to be a vol event.

Eurozone -ZEW survey (19:00aest) - watch the ZEW survey as a driver of the EUR, although it is expected to be quite a messy release, with the 'expectations' sub-component expected to decline slightly, while the 'current situation' should improve.

US - NFIB small business optimism (20:00aest), US (June) CPI (22:30aest) - consensus sits at +0.6% YoY, with core +1.1% YoY

Wednesday

UK - CPI (16:00aest) - consensus 0..0% MoM, 0.5% YoY, with core 1.2% YoY - the trend in cable is defined by the 5-day EMA, but clear indecision and a lack of commitment at this stage from GBP bulls to push this into the 200-day MA

US - June industrial production (consensus +4.3%), Beige book (04:00)

OPEC meeting - some belief that OPEC and Russia could cut production again given the continued worries about demand - WTI (XTIUSD) can't seem to clear $41.05 and finds sellers easy to come by into here. A closing break above here would appear material to a future bull trend. A move through Fridays low of $38.37 would open up a move into $34.32.

Thursday

NZ - 2Q CPI (08:45 aest) - the market expects inflation to decline by 0.5% in Q2, or 1.4% YoY. NZDUSD is pushing horizontal resistance at 0.6586 and needs a daily close through here. I've seen a 9-count on the TD set-up, so a close through the 5-day EMA opens up a move into 0.6500, which is the low implied range.

Australia - June employment report (11:30aest) - consensus expects 100,000 net jobs to be created (economists range is 175,000 to -30,000), although the unemployment rate is expected to tick up to 7.2% with the participation rate due to lift 30bp to 63.2%. The marquee domestic event risk for the AUD this week, although it's a lottery to forecast. We could easily see a short sharp move followed by a reversal, so not one I want to be involved in.

China - Q2 GDP (12:00 AEST) - Consensus 2.2% YoY/ 9.6% QoQ. Also, June Industrial production (also 12:00aest -+4.8%), retails sales (+0.5%), fixed asset investment (-3.4%).

UK - May jobless claims change, claimant count and ILO unemployment rate (16:00 aest) - consensus is that the ILO unemployment rate lifts 30bp to 4.2%.

Europe - ECB meeting (21:45 aest) - given what we saw in the June meeting this is expected to be a low vol risk. European data has been modestly improving and beating expectations butgiven the inability for inflation expectations to lift its unlikely Christine Lagarde will be anything but cautious. Risks to the EUR seem symmetrical.

US - retail sales (22:30aest) - consensus expects 5% growth in June, with the control group element growing 3.9%. Again, watch US Treasury yields here as it could impact the USD quite intently. We also see weekly jobless and continuing claims

Canada - Bank of Canada (BoC) meeting - The 200-day MA has held the downside move in USDCAD, and as we see from the vol matrix movers shy of the 200-day MA should see counter-traders into 1.3480. Markets are expecting a dovish narrative from the BoC, but should the USD bull kick in, on the week I am happy to fade rallies into 1.3700.

Friday

EU Council meeting - One of the big events for markets this week and possibly why EUR vols have lifted a touch. I'd say expectations of a formal agreement at this meeting on budgets, and more importantly, the EU's E750B Next Generation recovery fund are low given the public view of the 'Frugal Four' group of nations. However, traders are certainly expecting substantial progress to a deal. The EUR move will be driven on the belief that a deal is due in the next two months.

The meeting will run into the weekend, with the EU G20 Finance ministers meeting also playing gout over the weekend.

This article was submitted by Chris Weston, Head of Research at Pepperstone.