The rate of payrolls growth is expected to cool again in June, but once again, traders will be paying close attention to the wage metrics within the data to help shape expectations about whether the Fed will raise rates by either a 50bps or a 75bps increment at the July FOMC meeting. The jobs report is one part of the equation in forming these expectations, the other being the June CPI Data due next week. The data releases could also be influential in determining the course for rate hikes through the rest of this year; a recent dovish repricing of the trajectory of Fed rate hikes (on the back of recession fears) has been unwinding, and money markets now assign an approximately 50% chance rates will rise to 3.25-3.50% by year-end.

Expectations

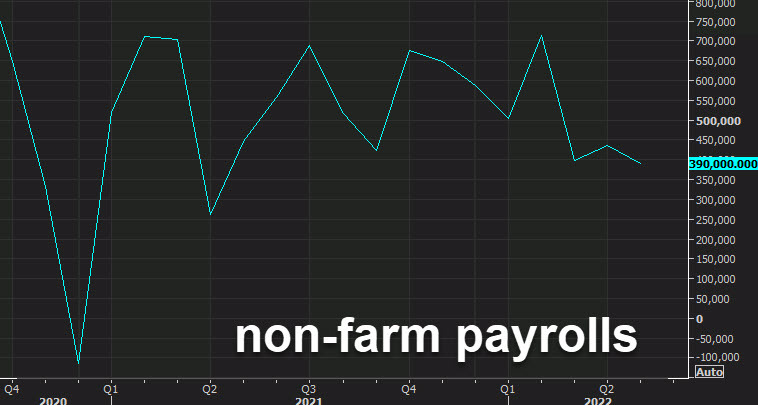

Analysts expect the rate of job additions will continue to cool in June, with the consensus looking for 268k payrolls to be added; that would be lower than May’s 390k, which is lower than recent averages too (3-month average 408k, 6-month average 505k, 12-month average 545k). Analysts see the jobless rate holding at 3.6% in June; the Fed’s recently updated economic projections see the unemployment rate ending this year at 3.7%, rising to 3.9% next year, and then 4.1% in 2024. Note, Fed Chair Powell in June said that unemployment at 4.1% would be a successful outcome and is still a historically low level, suggesting the Fed will be happy to allow unemployment to rise to this level as the Fed attempts to return inflation to target.

Average Hourly Earnings

As has been the case for many months now, traders will be carefully watching measures of wage growth for signs of how the ‘second round’ effects are faring. Average hourly earnings are expected to rise 0.3% M/M, matching the May rate; the annual measure is seen cooling to +5% Y/Y from 5.2% in May. The FOMC's June meeting minutes said that some contacts had reported that, because of previous wage hikes, hiring and retention had improved and pressure for additional wage increases appeared to be receding, while Powell at the June FOMC said we are not seeing a wage-price spiral but he did note wage growth is elevated.

Policy Implications

The Federal Reserve's recently updated economic forecasts acknowledge that aggressive rate hikes ahead will weigh on growth and the labour market. But officials have talked up the strength of the economy, and seem confident in their ability to tighten policy without causing significant damage to the labour market. Officials have noted that the jobs market is strong, demand for labour continues to outstrip supply, unemployment is near a 50-year low while job vacancies are at historical highs, and there is elevated nominal wage growth. Officials have recently been suggesting that the debate in July will be between 50bps and 75bps, and any upside surprise in the wages data will embolden calls for the Fed to raise rates by 75bps again on July 27th. Currently, money markets are assigning an approximately 85% chance that rates will be lifted by the larger increment, but if this metric was to post a downside surprise, it could help pricing tilt back into the 50bps bucket. It is also worth keeping in mind that Fed officials decided to go with a larger-than-guided 75bps rate hike in June after the hotter-than-expected May CPI data; accordingly, next Wednesday's CPI Report for June will also play an instrumental role in setting policy expectations for the July meeting. Some have suggested that the jobs data and inflation report might end up having more of an impact on pricing beyond the July meeting. Amid the recent growth fears, market pricing for rates to end this year between 3.25-3.50% diminished to the point that 3.00-3.25% was a more likely outcome; however, in recent sessions, we have seen the implied probability of a move to 3.25-3.50% rise and is now about 50/50.

This article originally appeared on Newsquawk get a free seven-day trial via ForexLive here.