Via eFX comes a client note from Deutsche Bank with outlooks and forecast for 2016 on euro, yen and sterling

GBP/USD:

"In 2016, the GBP is likely to remain vulnerable most obviously

against the USD. The pound in particular should suffer from a mix of

fiscal contraction constraining the BOE tightening cycle, making a C/A

deficit of near 5% of GDP more difficult to finance, most especially in

the face of 'Brexit' uncertainties. In 2016/7, Cable is expected

to test and likely break the 1.35 - 1.40 bottom end of the range that

has prevailed for 30 years," DB projects.

USD/JPY:

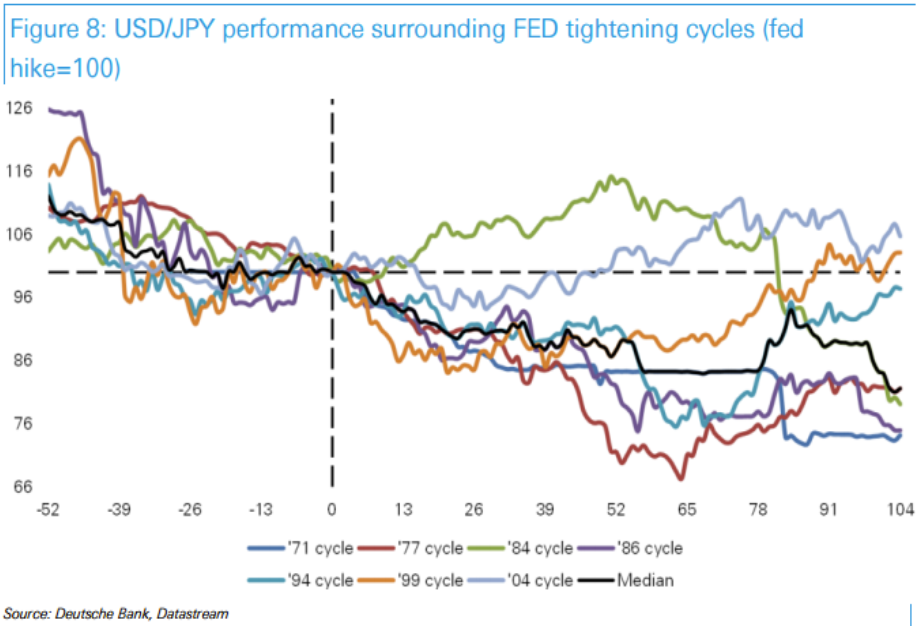

"We anticipate that when the USD shows toppish tendencies, the JPY

will take the lead, in much the same way is it was at the forefront of

the USD resurgence that started in late 2011. Even if the yen does not

quite conform to the past pattern of strengthening in Fed tightening

cycles, the yen will outperform almost all other currencies barring the USD in 2016, with a USD/JPY peak just shy of Y130," DB argues.

EUR/USD:

"2016 year-end forecasts have changed slightly, while end-2017 forecasts are largely unchanged. EUR/USD is now forecast at 0.95 at the end of 2016,

up from our original 0.90 forecast, in recognition of: i) some

prospective impact that risk factors like China will have in restraining

Fed expectations holding back the USD versus the majors as described

above; and, ii) EUR/USD is set to end 2015 slightly above our original

projections, setting a higher EUR/USD starting point for future

forecasts," DB adds.