Forex news for Asia-Pacific trade on December 2, 2019:

- China Caixin November manufacturing PMI 51.8 vs 51.5 expected

- Optimism about phase one China deal 'premature, if not misplaced' - report

- Australia November CoreLogic house prices +2.0% m/m vs +1.4% prior

- China continues to insist tariffs be rolled back as part of Phase One trade deal

- New Zealand Treasury says growth likely to fall below budget forecasts

- PBOC Governor Yi warns 'downturn will stay for a long time'

- Australia Q3 inventories -0.4% vs -0.2% expected

- Japan final November Jibun Bank manufacturing PMI 48.9 vs 48.6 prior

- Australia November ANZ job advertisements -1.7% m/m vs -1.0% prior

- Australia November building approvals -8.1% vs -1.0% m/m expected

- Australia Melbourne Institute inflation +1.5% y/y vs 1.5% prior

- UK election: Conservatives have 9 point lead in Survation poll

- Japan Q3 capital spending +7.1% y/y vs +5.0% expected

- CBA Australian final manufacturing PMI 49.9 vs 49.9 prelim

- New Zealand Q3 terms of trade +1.9% vs +0.7% expected

- Australia AiG performance of manufacturing index 48.1 vs 51.6 prior

Markets:

- Gold down $4 to $1459

- WTI crude oil up 88-cents to $56.05

- Nikkei 225 up 1.0% to 23527

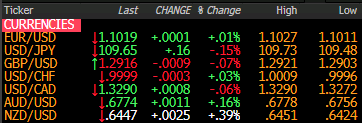

- NZD leads, JPY lags

The kiwi dollar is showing some lift to start the week as better risk sentiment takes hold despite the latest downer on China-US trade. For NZD specifically, the Q3 terms of trade report was btter than expected as export prices rose. The China PMIs were also strong and that's helped to lift NZD/JPY above 70.70.

Yen crosses more broadly have strengthened with USD/JPY edging above Friday's best level to a new six-month high. After starting near 109.50 the pair rallied to 109.70 as Tokyo ramped up for the week.

Cable is soft at 1.2916 after falling as low as 1.2903 at the outset as more polls show Labour cutting into the Conservative lead.

The euro has been uneventful so far and the German political news hasn't reverberated but that could change once Frankfurt comes online.