Forex news for NY trading on February 8, 2018

- Attention traders of the S&P, your up move was wrong and is being corrected (officially)

- S&P, Nasdaq and Dow all close below 100 day MAs. Dow down over 1,000 points.

- New Zealand - ANZ Truckometer for January: +4.1% m/m (vs. prior -4.2%)

- BOC Wilkins: High household debt is biggest vulnerability to economy

- CBO estimates budget deal would cost $320B

- Crude oil looks to close below 50 day MA

- Do we get a headline "S&P, Nasdaq and Dow close below 100 day MAs" soon?

- While stocks run all over the place, bitcoin settles between hourly MAs

- Trump Admin. considering making it harder for foreigners to become permanent residents if they use certain public benefits

- Bank of Mexico raises benchmark rate to 7.5% from 7.25%

- EURJPY falls back below daily trend line. GBPJPY stalls the fall at the 100 day MA

- US auctions 30 year bonds at 3.121%. Above the WI price. the

- Feds Dudley: Clearly markets adjusting to quick global growth

- UK Davis: EU threat over Brexit transition "not in good faith"

- European stocks (US stocks) take it on the chin

- GBPUSD gives up more than 50% of the Carney/BOE gains

- Germany's 10 year hits 0.80% for the first time since September 2015

- Bundesbank Dombret: Doubts mutual recognition of UK/EU banking rules after Brexit can work

- Kashkari on Bitcoin: Stick with USDJPY and leave bitcoin to toy collectors

- Harker speaks to reporters after speech: Would like to see inflation overshoot

- Fed's Kashkari speaks on a panel. Does not know impact of tax cuts on businesses

- Mexico CPI rose 0.53% vs 0.50 expected

- The market is anticipating the next BOE hike to come in the May meeting

- More Feds Harker: Inflation still an open question

- BOE's Carney: Possible over next few years that global equilibrium interest rates could be increasing

- Canada December new housing price index 0.0% vs +0.1% m/m expected

- US initial jobless claims 221K vs 232K expected

- Fed's Harker: GDP to get a bit of a bump from tax bill this year

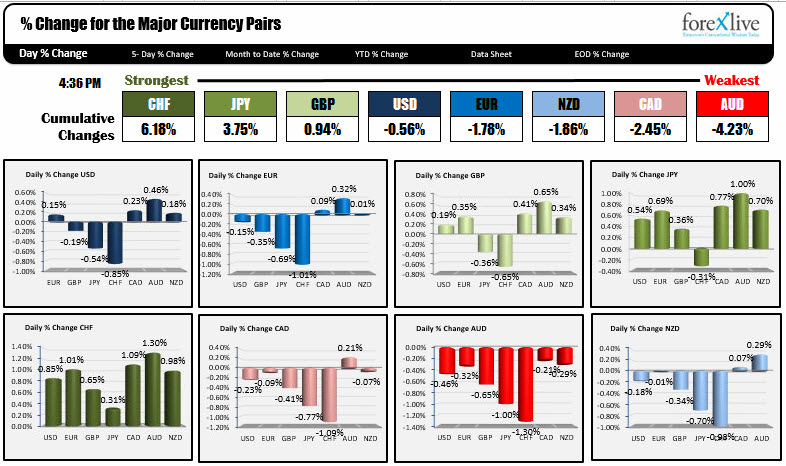

- A snapshot of the strongest and weakest currencies at the start of the NY session

In other markets near the NY session close:

- Spot gold unchanged at $1318.55

- WTI crude oil fell $-$1.33 or -2.15% at $60.46

- Bitcoin on Coinbase is trading up $100 at $8202. The 200 hour MA comes in at $8366 (and moving lower). A move above (and staying above) is needed for more upside potential.

- US yields are ending mixed: 2 year 2.105%, down -1.8 basis points. Five-year 2.541%, down -1.5 basis points. 10 year 2.825%, down 1.0 basis points. 30 year 3.127%, up 1.3 basis points The U.S. Treasury auctioned off 30 year bonds in a another sloppy auction at 3.121%. This week all three auctions were sloppy but the stock declines have been a counter force to the disappointing demand.

I know Forexlive is predominantly focused on forex, however, the stock markets stole the limelight today.

The European stock markets all closed with sharp declines. The Dax fell -2.62%. The French CAC fell -1.98%. The UK FTSE fell -1.49%.

Those declines were dwarfed by the major US indices.

- The S&P index fell -3.75%,

- The NASDAQ composite index fell -3.9% and

- The Dow industrial average fell -4.15%.

Moreover each of the major indices closed below their 100 day moving averages for the 1st time since November 4, 2016.

The catalyst?

The short volatility trade continues to be bantered about as the major reason. Too many traders are short volatility (which is a bullish trade). As volatility goes up (or as stocks go down), they are forced to buy volatility or sell stocks. It becomes a loop that can force a lot of pain. We are seeing a lot of pain.

Now, one close below the 100 day MAs does not necessarily make a trend. We also know that stocks - absent some real shock like housing collapsing, banking collapsing, dot.com bubble - will get bought over time. So finding the bottom is what traders should be looking for. However, the difficult thing is the valuation.

January did rise by >7% and that was after some pretty lofty 2017 gains. So there is that question of whether the market simply got too far ahead of itself.

The other catalyst is interest rates. Let's face it, in 2017 it was a Goldilocks scenario. Little inflation, a Fed that kept to the 3 hike plan and eased those hikes in. In 2018, we are seeing bonuses and raises. That is different than before. Does that justify more tightenings that slows the economy?

Tomorrow will be a key at least from a trading perspective. Let's also say, the low hanging fruit of 2017 where everyone became Warren Buffet, will likely not be duplicated in 2018 (or so it seems).

So what happened in the forex market?

The CHF suddenly became a safe haven again. The commodity currencies/risk currencies were shunned - led by the AUD. The USD was mixed with gains vs. the CAD, NZD and AUD, declines vs the CHF, JPY and GBP and near unchanged vs. the EUR. I guess that makes sense.

Fundamentally, the US released strong claims data. and Feds Dudley spoke somewhat hawkishly in an afternoon interview on Bloomberg. That did more to hurt the stocks than bother the forex market too much.

The other development in the forex market was the more hawkish BOE which helped to send the GBPUSD racing back above the 1.4000 level. However, when the pair sniffed the 200 hour Ma at the 1.4070 area, sellers entered and the rest of the day was spent falling back down. When the price got within a few pips of the close all the way down at 1.3875, the buyers stalled the fall. Nevertheless, the pair is ending the NY day just above 1.3900 (after moving as high at 1.4070).