From JP Morgan’s latest “FX Market Weekly: No vol, no problem?”

JPM says that despite the current low volatility we are seeing they are chalking it up “mostly to bad luck rather than permanently impaired markets and flawed frameworks”, and are “sticking with most core views. These include a mildly higher USD index by year end; a rangebound USD/JPY in Q2; about 3 cents lower on AUD, NZD and CAD in Q2; and significant dispersion across emerging markets FX”

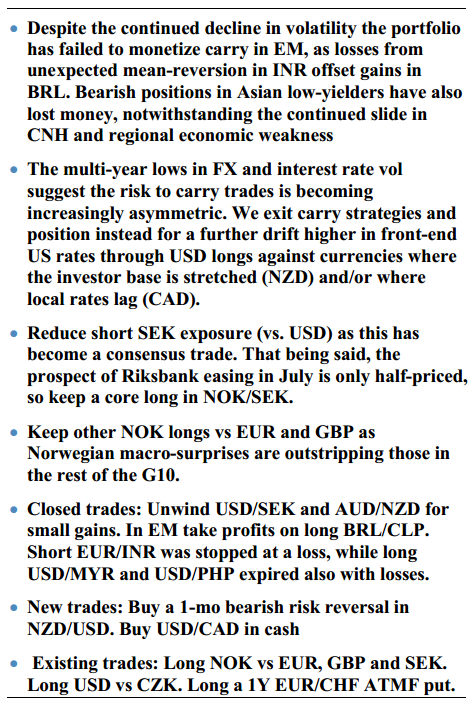

Their ‘Macro trade recommendations” are:

Our bias is to position for moderately higher US yields through selective dollar longs against currencies where leverage seems excessive, domestic fundamentals are turning less supportive (NZD in both cases) or where domestic rate expectations are expected to flat line and yield spreads to US to widen (CAD).

JPY has the highest beta to US rates this year, so may seem a natural vehicle for a better payrolls report, but we rule USD/JPY out-of-bounds until the impact of the consumption tax hike on the economy and the Nikkei can be better established.

Aside from carry the portfolio has been positioned for relative macro divergence (long NOK and AUD, short SEK and NZD). The SEK trade has become a little too consensus for our liking so we are trimming exposure ahead of a string of important Swedish activity releases next week (closing USD/SEK, holding NOK/SEK). The budding optimism towards AUD, meanwhile, was checked by the surprisingly tame CPI, so we close a AUD/NZD long and roll short NZD into NZD/USD instead (weak dairy prices, a more conditional outlook for RBNZ policy).