- US stocks close higher with the S&P index leading the way

- Biden/Xi: Discussed a face to face meeting in the future. Directed teams to follow up

- The CHIPs Act has passed in the House of Representatives

- Pres. Biden: No doubt that we expect to see growth slower compared to last year

- WTI crude oil futures settle at $96.42

- Yellen: US economy remains resilient in the face of headwinds

- US sells 7-year notes at 2.730% % vs 2.735% WI

- Xi told Biden with regard to Taiwan, that China firmly opposes Taiwan independence

- European equity close: Some blips but a strong finish

- Biden-Xi call readout from China: Had in-depth exchanges on Sino-US relations

- Weekly US natural gas inventories +15bcf vs +22bcf expected

- OPEC sources: Aug 3 meeting is set to keep output flat or raise slightly

- Biden: It's no surprise the US economy is slowing down as the Fed acts to lower inflation

- ECB's Visco: So far we don't have to worry about exchange rate

- US 10 year yield falls to the lowest level since April 14

- Strong bid in bonds questions Fed hikes. 10-year yield breaks key technical level

- Senior US administration official says optimistic about additional OPEC oil supply

- Canada average weekly earnings for May up 2.54% year on year

- US Q2 advance GDP -0.9% vs +0.5% expected

- US initial jobless claims 256K vs. 253K estimate

- The JPY is the strongest and the EUR is the weakest as the NA session begins.

- Germany July preliminary CPI +7.5% vs +7.4% y/y expected

The US GDP fell by -0.9% and as such, fell for the 2nd consecutive quarter (Q1 was down by -1.4%) putting the US in a technical recession.

Having said that the declines were a result of inventory. Continuing the "yeah, but...spin", inflation was also a major drag, subtracting -1% from the number.

Economists, Fed officials, politicians that are other not from the GOP side of the aisle, are rallying around the storyline that we can't be in a recession with employment near all time lows. GOP will blame Biden.

Admittedly, the employment picture has seen signs of deterioration (employment IS a lagging indicator). The weekly initial jobless claims came in at 256K (prior week was 261K). The low water mark in April reached 166K. IT is definitely on a slow but steady move to the upside.

Regardless of one's view, the market voted by ratching down yields, stocks moved higher under the idea that bad news is good news for inflation (less Fed down the road). The dollar tilted to the downside and gold and silver moved higher. For silver it broke higher, rising by $0.92 or 4.8% to $20.00 near the close for the day.

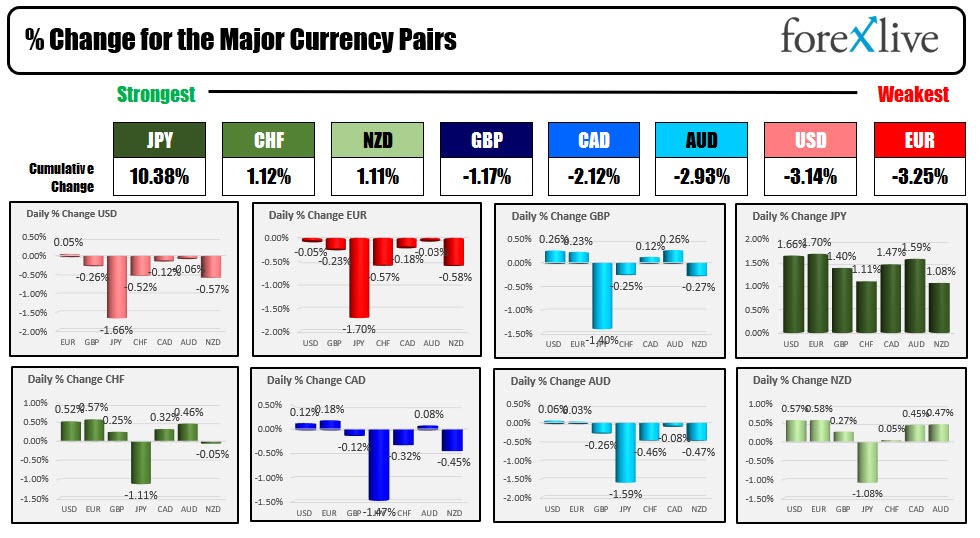

Looking at the strongest to the weakest, the JPY is ending the day as the runaway strongest of the majors, while, the EUR, USD and AUD are ending as the weakest (they are scrunched together).

The biggest mover vs the USDJPY which saw the dollar decline by -1.66%. The dollar fell by -0.57% vs the NZD and -0.52% vs the CHF. The USDJPY, USDCHF and NZDUSD are all closing at extreme levels for the day.

IN other markets:

- Spot gold is up $22.12 or 1.28% at 1756.27

- Spot silver soared by $0.92 or 4.85% to $19.99

- Crude oil saw prices come off highs at $99.83 to make a new low at $96.06 before moving higher. The price is at $97.27, unchanged on the day. OPEC+ sources said that production may increase by a small amount in September.

- Natural gas backed off on the day by -$0.40 to $8.16 after reaching a high on Tuesday at $9.399.

- Bitcoin is back above $24000 for the first time since July 20 at $24099.

In the US debt market, yields are sharply lower with:

- 2 year at 2.866%, -11.2 basis points

- 5 year at 2.701%, -12.8 basis point

- 10 year at 2.676%, -9.8 basis points