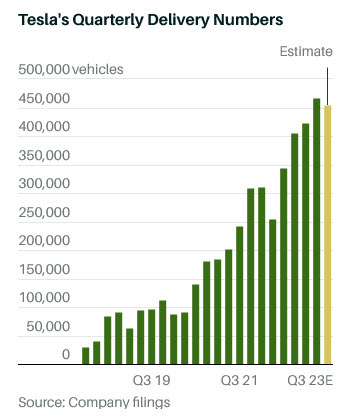

- Deliveries 435,059 vs 466,140 in Q2

- Production 433,059 vs 479,700 in Q2

The vast majority of Tesla sales are the Model 3/Y.

"A sequential decline in volumes was caused by planned downtimes for factory upgrades, as discussed on the most recent earnings call. Our 2023 volume target of around 1.8 million vehicles remains unchanged," the company said in the release.

Shares immediately fell about 2% and are down 3.25% in the premarket.

Wall Street estimates for Tesla deliveries were all over the place for this report as the company coaxed estimates lower in the past month. A few weeks ago, the consensus was at 473K units but that's been pared down to 456.7K with some as low as 438K and as high as 511K.

Last quarter, Tesla delivered about 466K vehicles so this would be falling quarterly deliveries, which has happened to TSLA from time to time.

Last week, Bloomberg was out with a review of Mercedes-Benz's level 3 self-driving technology and they said it's better than TSLA's, though it's only out at slower speeds.

Looking ahead, the estimates for 2024 include a 27% increase in revenue, which is going to be an awfully tough bar to hit given high interest rates, price cuts, sales that were flat q/q and the stalled launch of the cybertruck. Five-year Treasury yields are 7.9 basis points higher to 4.68%.

Of course, the market could always go from 71 x earnings currently to 100x, why not?

The chart has been consolidating in the $210-$300 range since June.

Tesla plans to report Q3 earnings on October 19.

Earlier, electric-vehicle maker Rivian announced production above estimates but shares are down 4.5% in the premarket.