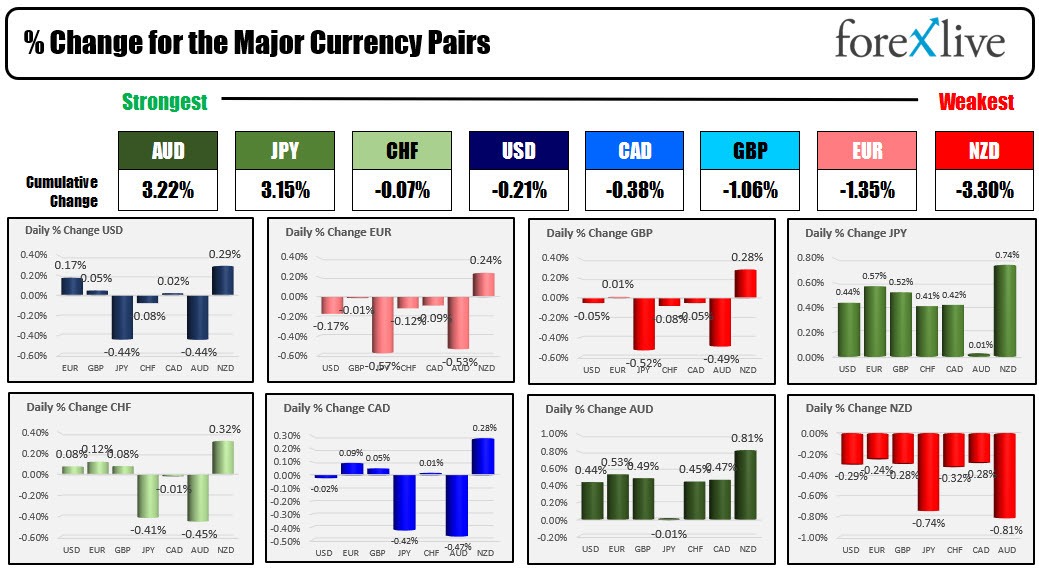

As the NA session begins, the AUD is the strongest and the NZD is the weakest. The two countries released their 4Q CPI data in the new trading day. New Zealand was higher than expectations at 1.4% vs 1.3% but Australia was even higher with a gain of 1.9% vs 1.6% expected. That took the YoY to 8.4% from 7.3% last month. Inflation is not slowing there.

The US dollars mixed with the clients mostly versus the JPY and AUD, and gains vs the NZD and EUR.

In other news, Microsoft announced earnings and initially the reaction was a move to the upside with gains of about $11 on the day at around $253. After the earnings call came out, the guidance was less than expectations and the stock fell sharply. It is currently trading down -6.00 or -2.50% at $236.

In other earnings news this morning:

- Boeing fell short on the top and bottom line. Earnings-per-share $1.06 versus plus $0.26. Revenues $19.98 billion versus expected $20.38 billion

- Abbott Laboratories beat on the top and bottom line. EPS $1.03 versus $0.92. Revenues $10.1 billion versus $9.67 billion expected

- AT&T had mixed results. EPS B at $0.61 versus $0.57 expected. Revenues were marginally lower $31.343 billion versus $31.39 billion expected

German Ifo data came in as expected 90.2 for the third straight gain. Last month the index came in at 88.6

The Bank of Canada will announce their rate decision today at 10 AM ET. The expectations are for a 25 basis point rise but Adam Button points out that the BOC is not afraid to go against the market pundits (CLICK HERE for the post/preview).

In other markets, the snapshot of the market is showing:

- Spot gold is down $10.25 or -0.53% in $1926.81

- Spot silver is trading down $0.19 or -0.80% at $23.45

- WTI crude oil is trading unchanged at $80.12. The private inventory data last night showed a larger than expected build (once again) with crude inventories up 3.378 million barrels. Today the EIA expectations are for crude stocks to rise by about 1 million barrels. Gasoline inventories rose 0.620 million versus expectations of a gain of 1.767 million today from the EIA

- Bitcoin is trading back below the $23,000 level at $22,690

The premarket for US stocks, the major indices lower after mixed results yesterday. The Microsoft news and other disappointments (Boeing) are pointing to a lower opening:

- Dow Industrial Average is trading down -190 points after yesterday's 104.4 point rise

- S&P index is down down -30 points after yesterday's -2.88 point decline

- NASDAQ index is down -138 points after yesterday's -30.14 point decline

Tesla reports earnings after the close with earnings estimated at $1.15 down from $2.54 a year ago. IBM will also release.

In the European equity markets, the major indices are trading lower

- German DAX -0.44%

- France's CAC -0.38%

- UK's FTSE 100 -0.21%

- Spain's Ibex -0.27%

- Italy's FTSE MIB -0.36%

In the Asian-Pacific market, China remains on lunar holiday with the markets closed:

- Japan's Nikkei rose 0.35%

- New Zealand 50 index rose 0.52%

- Australia's S&P/ASX index -0.30%

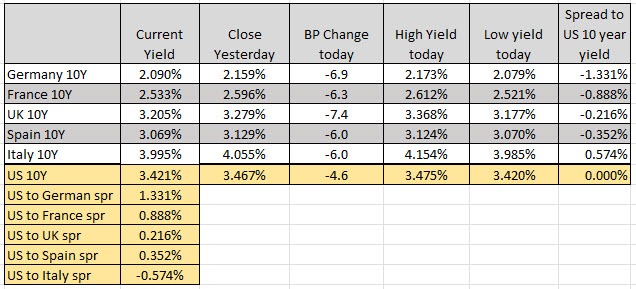

In the US debt market yields are lower:

- 2 year 4.139%, -1.4 basis points

- 5 year 3.543% -3.8 basis points

- 10 year 3.423% -4.4 basis points

- 30 year 3.579% -4.1 basis points

In the European debt market, the benchmark 10 year yields are moving lower as well