Private Capital Expenditure survey from the Australian Bureau of Statistics for the October - December quarter.

Of interest in the data is both

- the backward looking data (this is the 'headline' business capex for the quarter just passed, the Bloomberg survey has median expectations at +1.0% while Q3 was also +1.0%) which feeds into GDP data (due for Q4 next week from Australia)

- AND the forward foreword looking 'estimates' - today the focus is on 'estimate 5' for the year (2018/18) and also on 'estimate 1' for 2018/19 capex.

I posted a preview of this yesterday, here:

A couple more previews now, any bolding is mine (headline, estimate 5 and estimate 1 all bolded).

Via ...

Westpac:

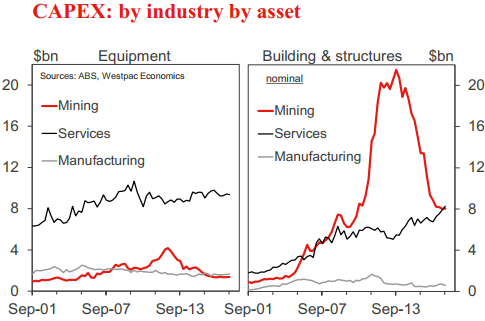

- Business capex spending turned the corner in 2017 with the mining investment wind-down largely complete and with the emergence of an upswing in investment by the non-mining economy.

- Equipment spending appears to have emerged from the soft spot during the second half of 2016, which was associated with uncertainty around the July Federal election. We anticipate a further 1% increase in the December quarter, lifting annual growth to 4%.

- Building & structures capex spending while still at a relatively low level has also moved higher in 2017. There has been some resilience in mining (as the remaining gas projects under construction are completed) and as commercial building activity advances.

- For Q4 we anticipate an outcome of around +0.6%qtr, 4.4%yr (factoring in a 3.4%qtr rise in non-residential building and a 1% decline in engineering).

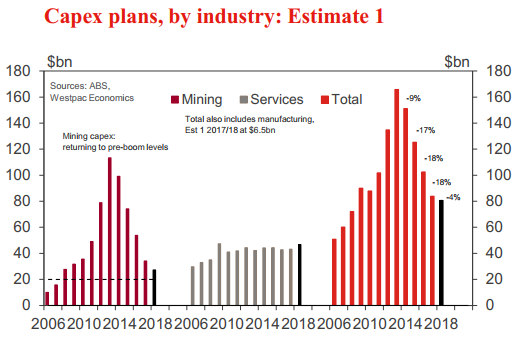

- Estimate 4 of capex plans for 2017/18 is $108.9bn, 1.6% above Est 4 a year ago, an improvement on -2.4% for Est 3. Based on average realisation calculations, we estimate that Est 4 implies capex spend in 2017/18 will be broadly unchanged from 2016/17. Mining capex spend will be down on the year prior offset by an increase in the service sectors, centred on a rise in building activity.

- Est 5 (with a potential upgrade to around $112bn) will likely confirm this consolidation in 2017/18 at a time of improving conditions globally but an uneven expansion domestically, with consumer spending the source of weakness.

- This survey update, conducted in January and February, will include the initial estimate (which is often unreliable) of capex spending for 2018/19. Potentially, Est 1 could be in the order of $82bn, 1% above Est 1 a year ago, as mining capex forms a base. Service sector intentions will be of particular focus - a lack of a clear signal at this early stage would not surprise (capex plans tend to firm up later in the piece).

CBA:

There are three key figures in ... capex survey

- (i) Q4 2017 actual spending;

- (ii) 2017/18 expectations (5th estimate);

- and (iii) 2018/19 expectations (1st estimate).

Markets will focus on the forward looking expenditure plans, particularly the first cut of 2018/19 spending intentions.

- First estimates for spending plans can vary significantly from actual spending. A comparison of previous first estimates with actuals shows that non-mining firms will almost always underestimate their capex plans at first stab. But the magnitude of the miss can vary greatly in any given year. As the economic landscape changes, capex spending plans evolve accordingly. The first estimate is often revised up sharply if demand lifts. Mining firms, on the other hand, have tended to more accurately estimate their capex plans over the past few years - basically since the peak in the investment boom.

- Our forecast is for nominal capex, as measured by the survey, to lift by 4% in 2018/19 (comprised of a 7% increase in non-mining investment and a 2% fall in mining capex). For that to materialise, we are looking for the first estimate of 2018/19 capex spending plans to come in around $84bn.

We would interpret a figure above $57bn for non-mining spending plans as a good outcome as it would imply a respectable pickup in capex outside of the resources sector (note that our pick of $58bn would be a strong outcome). Mining continues to fall as a share of total capex and the drag on growth from falling resources investment is largely done.

The last reading from three months ago implied a small of around 1% in nominal capex this financial year. The detail suggests a fall in mining capex of 22% and a healthy 10% increase in non-mining investment. Here we note that the capex survey only captures around 60% of business investment as per the national accounts. The survey excludes a number of large and important industries which include agriculture, health and education.

We expect the actual volume of Q4 capex to rise 1.7% after a 1.0% increase in Q3.

- Such an outcome would leave annual growth 5.2% higher.

- The actual spending data will help firm up our estimates of Q4 GDP growth (due 7 March). Global growth has picked up and local employment growth has been strong. On balance, these factors point to upside risk on our 2017/18 capex expectations. The risk to our 2018/19 forecast, however, is to the downside given there are a few LNG projects set for completion in 2018/19.

---