Forex news for Asia trading Friday 11 September 2020

- Japan sends mixed signals on a sales tax hike

- Japan - UK trade talks today - aim to reach broad agreement

- The BOJ has slipped in a meeting on 'market operations' on October 20

- US inflation data for August is due on Friday 11 September 2020 - preview

- ANZ on Japan's next Prime Minister and what it means for policy

- PBOC sets USD/ CNY reference rate for today at 6.8389 (vs. yesterday at 6.8331)

- FX option expiries for Friday September 11 at the 10am NY cut

- ANZ on gold - the supportive factors and forecast into next year

- Tokyo lowered its coronavirus alert to 3, from 4 as new daily cases have fallen.

- Japan PPI 0.2% m/m (expected 0.2%)

- Heads up for EUR traders - ECB's Lane speaks on Friday (the guy who pricked the euro rise)

- Will US policy toward China change under Biden ... probably not

- New Zealand Food Price (inflation) forAugust: +0.7% m/m (prior +1.2%)

- New Zealand - BusinessNZ manufacturing PMI for August: 50.7 (prior 58.8)

- Goldman Sachs on the European Central Bank statement on the EUR

- Trump says there will no extension to the TikTok deadline

- COVID-19 - France posts a record near 10,000 new cases in 24 hours

- Canada says a sales tax is coming for tech giants

- New Zealand August home prices, sales activity, up

- Saudi Aramco has raised domestic fuel prices

- Trade ideas thread - Friday 11 September 2020

Asia's Friday session has been devoid of news and data to shift FX rates about. Nevertheless there has been a small loss of ground for the US dollar pretty much across the board on a retracement of the US session moves.

EUR/USD hit lows very early(late US afternoon) under 1.1815 before ticking slowly higher to 1.1840. AUD, NZD, GBP, CAD - all followed a similar pattern against the USD.

USD/JPY and USD/CHF are little changed.

Ahead for the rest of Friday is the US CPI data, which could well impact on equity sentiment if its seen as providing any reason for more or less from the Federal Reserve, it could be yet another day of gyrations for US stocks. Also on the agenda is an appearance from ECB head economist Phillip Lane, the chap who gave EUR a kick lower a week ago or so.

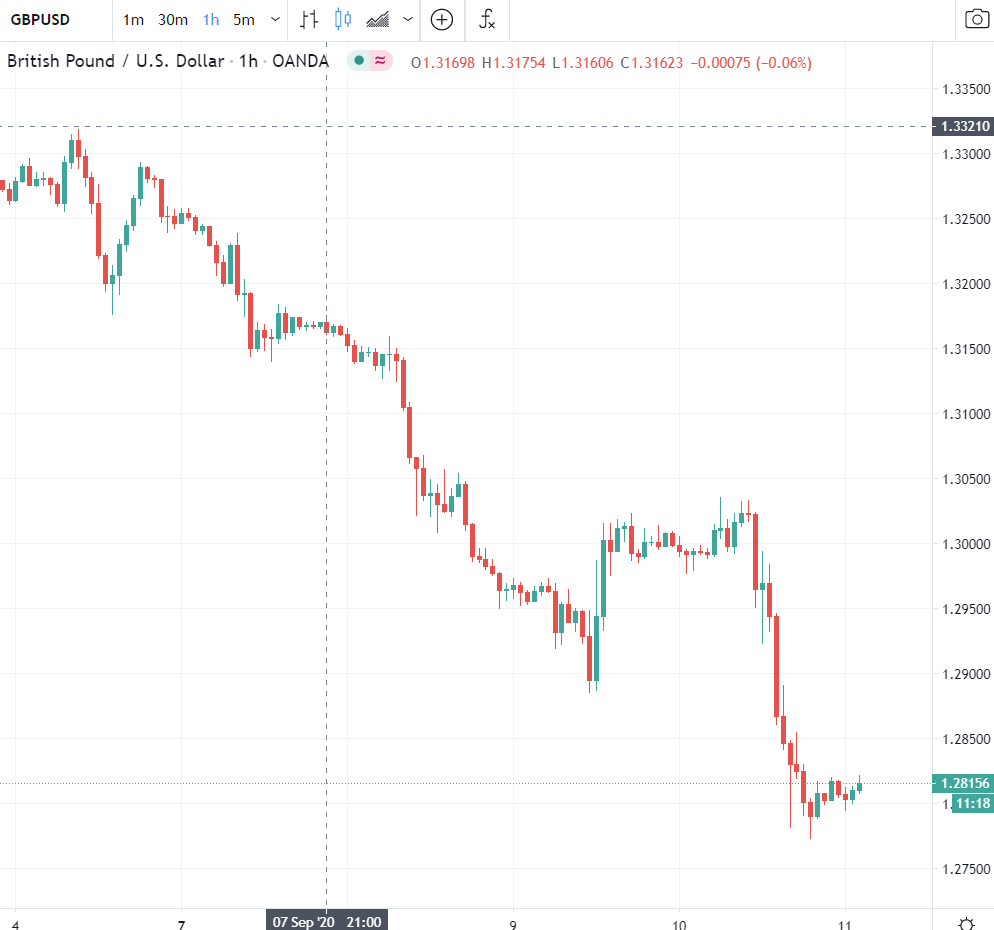

Finally, please join me on Monday morning for the usual (very) early opening of the new FX week. Last Monday (Sep. 7) we had a slew of Brexit trade talk related headlines which set the tone for the entire week on GBP as it slid, and slipped, and slid and slid some more. Not every Monday AM is as impactful, of course, but it never hurts to stay in touch.

Weak week for GBP: