Targeting unemployment is a symptom of the politicisation of central banks

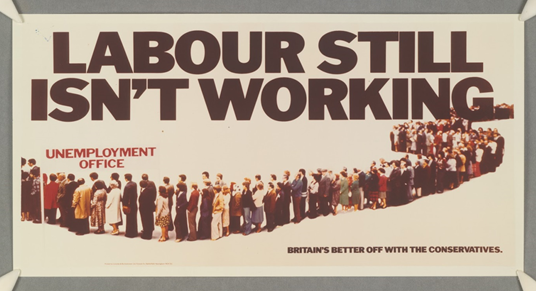

In 1982 unemployment in the UK hit three million. Thatcher had swept to power three years before with the help of the iconic Saatchi election poster:

Unemployment was the issue of the day, so much so that a pop group called themselves after the UK form for the jobless – UB40. And so for a reminiscence of those times, here’s Kingston Town:

For obvious reasons, unemployment has always been the most politically sensitive economic statistic. Some of the most powerful images from the Great Depression are of the desperate unemployed:

Unemployment is the top figure that the electorate care about especially in recessionary times. If voters lose their jobs, it is the statistic they directly feel in their pockets. And so with the growing politicisation of central banks, it should be no surprise that it is also the figure that both the American Federal Reserve and the UK’s Bank of England have decided to base their monetary decisions upon.

I am deeply sceptical for four reasons.

1) Firstly, because an economy is much more complex than just one data point. According to the statistician Nate Silverman “the (US) government produces data on literally 45,000 economic indicators each year. Private data providers track as many as four million statistics.” That is an awful lot of data deemed to be necessary to try and understand the US economy. Picking one point – unemployment – to assess the health of the economy is like a doctor looking at temperature alone to assess the health of a patient. In reality adDoctor uses many data points; heart rate, blood pressure, symptoms, blood tests etc. But Bernanke and Carney are going back to the medical practices of old relying on just one input to cure their patients. Understanding how a human body works is difficult enough but understanding how something as complex as a multi-trillion dollar economy works almost impossible. Simplifying that complexity to just one figure, unemployment, is ridiculous.

2) Secondly the UK demonstrates that economists did not understand the drivers of unemployment after the great financial crash. There has been much bewilderment at the strength of the employment data relative to the weakness of the economy – the productivity conundrum. Large increases in unemployment were almost unanimously forecast (based on models and previous recessions) and yet it did not happen. The jobless rate has been much lower than even the coalition had hoped. Since the start of the recession at the beginning of 2008 to the 1Q of 2012, employment fell by less than 1% and yet GDP fell 4%. Why?

It is clear that behaviour has changed in this cycle. Some evidence suggests that managers decided not to sack their workers but kept them on the payroll on reduced hours. There was an increase in part time working and an increase too in temporary contracts. Is this greater labour market flexibility due to changes to labour law, or an increasing employee willingness to accept cuts given the fear surrounding the crisis? No one quite knows.

The UK’s Office for National statistics has written about this productivity conundrum and in it there is a graph that shows quite how different the experience in 2008 has been to any of the past recessions in the UK (1973, 1980 and 1990). A truly startling difference that no one forecast.

Economists do not understand how unemployment was acting during the recession, and so are unlikely to be able to forecast or understand how it will act during the recovery. This makes using it as the one indicator on which to base monetary tightening dangerous.

3) The third reason I do not like using unemployment as the determinant of monetary policy is that is the jobless rate is highly dependent on government policy. Labour law, labour market reforms, immigration, minimum wage, the benefit system, educational levels, etc. All of these affect the jobless rate and yet are determined by government policy. Also important is the structural level of long term unemployment. Those that even if interest rates were 0% for ever, would never get a job. Any estimate of this level is a guess at best.

The Fed and the Bank of England are targeting a variable that they only partly control. Much of the unemployment rate is dependent on government policy. Any motivational speaker will advise to only set achievable goals, losing weight, yes, but increasing height, no. Thinner is achievable, taller isn’t. By setting a target they only partly control, the Fed and the Bof E are risking trying to grow.

4) Lastly, like all economic statistics, unemployment data is always revised. The quality of the initial estimates is generally poor. In particular the non-farm payroll figures from the American Bureau of Labor Statistics, are prone to large revisions. For example the initial estimate of the number of jobs added in August 2012 was 96,000 for the month but by the third release that was revised to 192,000. The unemployment rate is not as problematic but there are occasional large revisions.

The Federal Reserve and the Bank of England have targeted unemployment due to political necessity and the need to have a clearly communicated and easily understood objective. Nevertheless, I have reservations; focusing on just one statistic which is poorly understood, partly out of the control of central bankers and subject to substantial revisions.

And I am not the only women to fear reliance on just one data point in setting monetary policy. In a speech to the Swedish Trade Union Conference in January 2012, Ms Barbro Wickman-Parak, Deputy Governor of the Sveriges Riksbank, said “I do not consider that there is a single measure that can or should be held up as the only measure that we should adjust monetary policy to.”

Great (women’s) minds think alike.