A long piece via eFX on Goldman Sachs FX forecasts on euro and yen

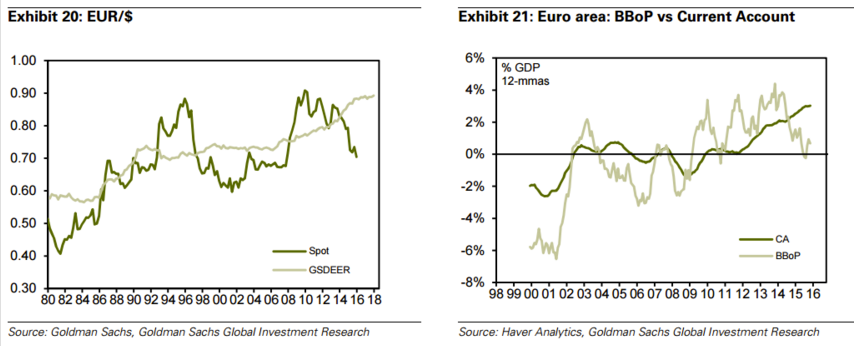

Euro: FX Forecasts: We maintain our EUR/USD forecasts of 1.04, 1.00 and 0.95 in 3, 6 and 12 months, which we reverted to on January 21. This implies EUR/¥ at 127, 125 and 124 in 3, 6 and 12 months.Motivation for Our FX View: We continue to believe that EUR/USD and EUR/GBP will move substantially lower on diverging growth and monetary policy outlooks. The EUR has already weakened significantly over the last 18 months, but we think this trend has a long way to run. In particular, we see a couple of longer-term fundamental forces at work. First, the flow picture should turn increasingly EUR-negative as Euro area residents send funds abroad and reserve managers allocate away from the EUR. Second, we think there is a structural element to disinflation in the periphery as it continues to improve competitiveness compared with the core of the Euro area. As a result, our view is that inflation will be slower to pick up than during a normal cycle, in line with projections from our European team, which show HICP inflation reverting to target only slowly. This will keep ECB policy accommodative, maintaining downward pressure on the EUR. Monetary Policy and FX Framework: The ECB is a strict inflation targeter and has recently made more explicit its inflation-based forward guidance. The Euro floats freely. FX policy responsibility is shared between the ECB and Eurogroup. Growth/Inflation Outlook: Reflecting lower oil prices and more aggressive monetary policy, we expect resilient growth in 2015. We forecast that the Euro area will expand by 1.7%yoy in 2016, a modest improvement over 1.5% growth in 2015, but substantially above the 0.9% recorded in 2014. Nevertheless, we expect core inflation to rise only slowly. Our forecast for core inflation of 1.0% in 2016 is well below the ECB staff's 1.3% projection. We expect core inflation to rise slowly from just below 1.0% to 1.7% by end-2018. Monetary Policy Forecast: In December, the ECB cut its deposit rate by 10bp and extended its QE programme until March 2017. The downside risks to its forecast have since increased, and in January the ECB made it clear that it would review and possibly reconsider its monetary policy stance as soon as March. We expect the ECB to extend its QE programme at the current pace through September 2017 and cut its deposit rate by another 10bp. Our inflation projections, which show a more moderate increase than the ECB staff forecast, suggest that a decision to reduce policy accommodation remains a long way off. Fiscal Policy Outlook: Fiscal policy has been highly contractionary in recent years, but turned more neutral in 2014. We expect it to remain close to neutral over the next several years. Balance of Payments Situation: The Euro area is currently recording a current account surplus of about 3% of GDP on a trend basis, leading to a slightly positive BBoP. Portfolio inflows have slowed, and there are signs that Euro area investors have started to buy more foreign assets. We expect that to continue. Things to Watch: Developments in the European sovereign situation, in particular the implementation of fiscal reforms and long-term fiscal and political reforms, remain the key risk in focus.

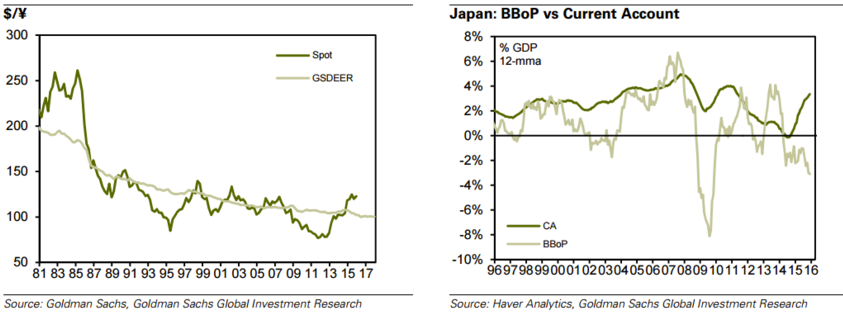

Japanese Yen: FX Forecasts: We maintain our USD/JPY forecasts of 122, 125 and 130 in 3, 6 and 12 months. This implies EUR/¥ at 127, 125 and 124 in 3, 6 and 12 months.Motivation for Our FX View: The BoJ surprised the market by introducing a negative interest rate at its January 2016 meeting. This will augment the Bank's ongoing QQE programme, which is increasing the monetary base by JPY80trn per year. A negative interest rate is a significant regime break for the BoJ, and at the same time it was keen to stress that the negative rate is not a substitute for additional asset purchases, but rather a third prong - in addition to quantitative and qualitative easing - in its policy stance. Overall, we think the BoJ's recent actions demonstrate that it is willing to innovate in its monetary policy measures and is committed to its price target. We think this continued policy divergence will continue to drive the JPY weaker against the USD. Monetary Policy and FX Framework: After adopting a 2% inflation target in 2013, the BoJ has changed its main operating target for monetary market operations for a monetary base control, from the uncollateralised overnight call rate. Open market operations are conducted such that the monetary base increases at an annual pace of ¥80trn. In January 2016, the BoJ introduced a tiered interest rate regime, including a bottom tier of -0.1%. The Yen is formally a freely floating currency, but the MoF is in charge of FX policy and has often intervened in the past. Growth/Inflation Outlook: GDP likely contracted in 2015Q4 and grew just 0.9% in 2015. We expect a small acceleration in 2016 to 0.8%. However, while the BoJ's new interest rate regime aims to stimulate capital expenditures, we have doubts this transmission channel will work. The fall in oil prices pushed inflation into negative territory for the first time since 2013. But weaker inflation is not just an oil story, as core of core is also likely to fall short of the BoJ's forecast. We believe the Bank of Japan needs to ease further to avoid losing inflation momentum. Monetary Policy Forecast: The BoJ is currently purchasing ¥80trn-worth of JGBs annually up to a maturity of 40 years and an average duration of between 7 and 12 years, as well as other assets such as REITs. The BoJ has committed to expanding its balance sheet until the price stability target of 2% is reached sustainably. Following its interest rate actions in January, we expect the BoJ to be on hold for a time to assess the impact of its new easing measures. If the inflation outlook were to deteriorate, we believe the most likely response would be further interest rate cuts. Fiscal Policy Outlook: The Japanese government announced its latest fiscal consolidation plan on June 30 and its medium/long-term outlook on July 22. We think it will be difficult to achieve these new targets given their optimistic growth assumptions. We expect government spending to grow 1.2% in 2015 and 0.8% in 2016. Balance of Payments Situation: The Japanese current account has improved substantially over the last year, partly owing to the decline in oil prices. Nevertheless, the BBoP has declined as a result of higher portfolio outflows. Things to Watch: On the one hand, we are watching for any signs that the economy is responding to ongoing monetary easing. On the other, we are watching for signs that the BoJ could start to waver on its inflation target.