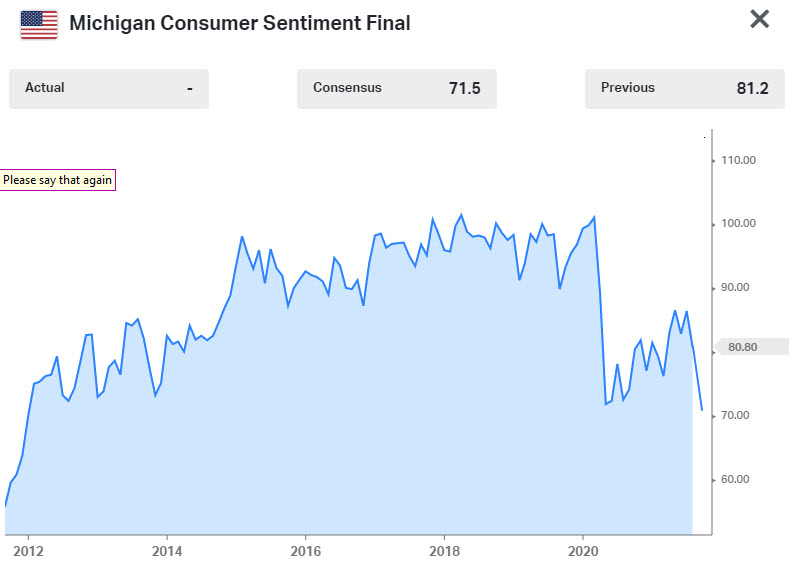

Consumer sentiment data form the University of Michigan

- Prior was 70.3

- Current conditions 77.1 vs 78.5 prior

- Expectations 67.1 vs 65.1 prior

- 1-year inflation 4.7% vs 4.6% prior

- 5-10 year inflation 2.9% vs 2.9% prior

This report drew intense interest last month when it collapsed through the pandemic lows. However the August retail sales report didn't mirror that weakness as it widely beat expectations.

The problem with this report is that it's increasingly a political barometer, which you can see when you break down sentiment by Democrats and Republicans.

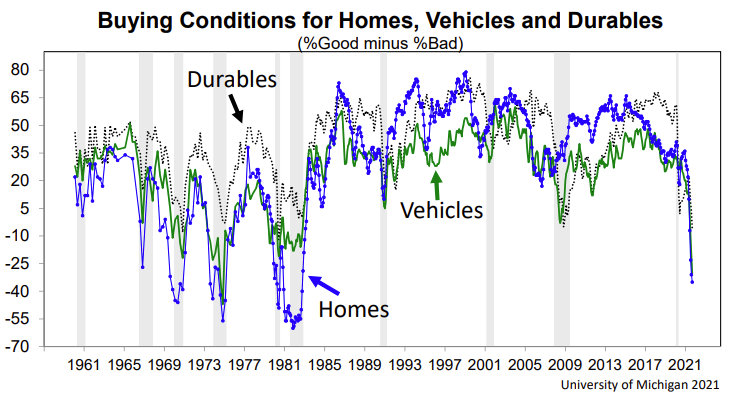

The Fed does look closely at the inflation expectations numbers though. The buying intentions data for homes, vehicles and durables is also instructive.

Here's the commentary in the survey:

The steep August falloff in consumer sentiment ended in early September, but the small gain still meant that consumers expected the least favorable economic prospects in more than a decade. Just two components posted additional declines: buying attitudes for household durables fell again in early September to a low reached only once before in 1980, and long term economic prospects fell to a decade low. The decline in assessments of buying conditions for homes, vehicles, and household durables left all three near all-time record lows (see the chart above), with the declines due to spontaneous references to high prices. Some observers anticipated that the early August plunge in confidence would quickly disappear since it was driven by emotions. Emotions have long been known to speed responses, the so-called fight or flight response, which was the adaptive function they performed in early August. Many other sources of economic data have since shifted in the same direction, and point toward slower growth in consumer expenditures and purchases of housing to the end of 2021.

There are at least three potential reactions to inflation. Consumers have initially reacted by viewing the rise in inflation as transitory, believing that prices will stabilize or could even fall in the future. As a result, postponing purchases is seen as a viable strategy. This implies a slowdown of spending in the months ahead and a more robust rebound later in 2022. The main alternative is that inflation will not be transient but will rise further due to an unprecedented expansion in fiscal and monetary policies. The resulting rise in inflationary psychology will lessen resistance to rising prices and stiffen demands for increased wage gains. This reaction takes a long time to fully develop, and is contingent on significant increases in long-term inflation expectations, which have yet to be observed. The final alternative is that consumers may believe that the most effective strategy to maintaining their purchasing power is to emphasize increases in their incomes, net of taxes and transfers. The effectiveness of pandemic transfers were shown by their successes in offsetting hardships among those most vulnerable to economic disparities. Transfers to offset the inflationary erosion of living standards could be justified in a similar manner.