Forex news for Asia trading for Friday 27 November 2020

- North Korea executed an FX dealer in Pyongyang because of the rapid drop in the exchange rate

- Here are 3 reasons the FOMC will further ease policy next month

- North Korea has ordered its overseas missions not to antagonise the US

- FX option expiries for Friday November 27 at the 10am NY cut

- China Foreign Ministry Spokesperson welcomes Asia's RCEP trade deal

- ECB's Panetta says there should be no doubt on the Bank's inflation commitment

- RBA monetary policy meeting next week - preview (spoiler - no change expected)

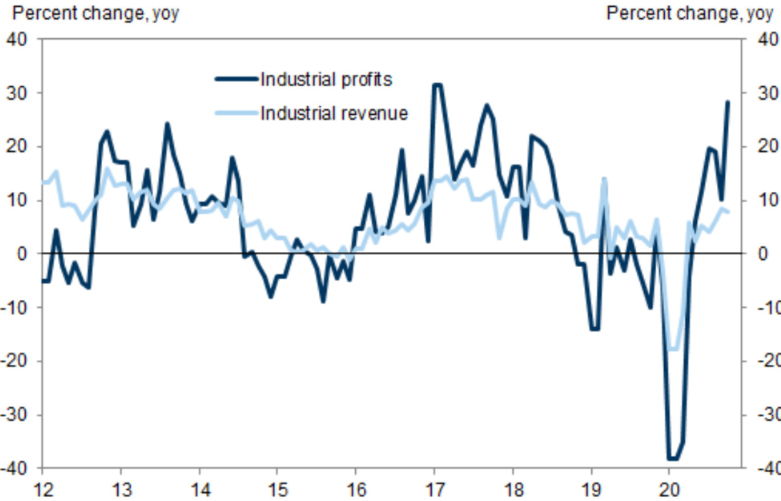

- China Industrial Profits for October +28.2% y/y (prior +10.1%)

- PBOC sets USD/ CNY reference rate for today at 6.5755 (vs. yesterday at 6.5780)

- China to impose anti-dumping duties on Australian wine

- Japan's ruling party calls for more support from coronavirus-hit firms

- JPMorgan's S&P target is 4500 (year-end 2021)

- NZ Treasury highlights an upside risk to economic growth

- The UK is moving to get Oxford-Astra COVID-19 vaccine drug approved faster

- South Korea new coronavirus cases are above 500 for another day

- Brexit - EU decision on market access for UK banks, financial firms will not be before January 1

- Brexit (ICYMI) - EU and UK negotiators will meet in London this weekend ... but there's a but

- Tokyo inflation data for November - Headline CPI -0.7% y/y (expected -0.5%)

- 80 ships and counting - Australian coal ships refused entry to China ports

- Trump says COVID-19 vaccine delivery to begin next week

- ANZ maintain their 12-month target for gold, higher at $US 2,100/oz

- Trade ideas thread - Friday 27 November 2020

- ICYMI - PBOC says will keep China's yuan rate flexible, allow market to determine rate

- BoC's Wilkins comments now - says the 2% inflation target remains very relevant

- More from Macklem - negative rates would not be terribly helpful at present

- New Zealand – ANZ Consumer Confidence Index for November -1.7% m/m (prior +8.7%)

USD/JPY lost ground during the session here and as I post is making fresh lows for the day under 104. There was no specific catalyst visible apart from selling flows into month end. Other currencies have been pretty much flat against the USD (minor chop only) but have just seen some buying (USD selling) in the hour or so to take currencies net up on the day. The rise in the Australian dollar came despite a further worsening of the coal ban from China and fresh imposts on Australian wine (see bullets above).

The data of note was out of China, October industrial profits surged and have taken the YTD figure into the positive (after a bad pandemic-hit year of course).

Goldman Sachs chart of China industrial profits: