Highlights of the September 2021 non-farm payrolls report:

- Prior was 235K (revised to +366K)

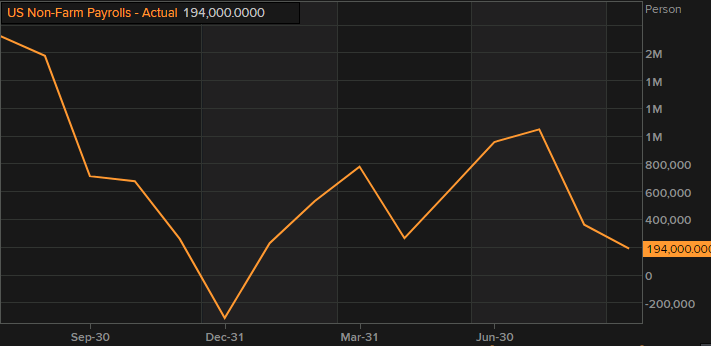

- Two month net revision +194K

- Unemployment rate 4.8% vs 5.1% expected

- Prior unemployment rate 5.2%

- Participation rate 61.6% vs 61.7% expected (was 62.8% pre-pandemic)

- Prime age participation to 81.6% vs 81.8% prior (83.0% pre-pandemic)

- Prior participation rate 61.7%

- Underemployment rate 8.5% vs 9.0% expected (8.8% prior)

- Average hourly earnings +0.6% m/m vs +0.4% expected

- Average hourly earnings +4.6% y/y vs +4.6% expected

- Average weekly hours 34.8 vs 34.7 expected

- Change in private payrolls +317K vs +455K expected

- Change in manufacturing payrolls +26K vs +25K expected

- Long-term unemployed at 2.7m vs 3.2m prior

- The employment-population ratio, at 58.7% vs 58.5% prior (61% before pandemic)

The revision to August upwards by 131K and the better unemployment rate take a bit of the sting out of the report but it's not a great number by any stretch.

Another notable detail is the bit improvement in the number of long-term unemployed (those jobless for 27 weeks or more) which decreased by 496,000 in September to 2.7 million. That had been stuck at high levels.

On the wage side, the wages numbers were a tad hot and that fits in with anecdotes. We will get the JOLTS data next week.

In August the 'leisure and hospitality' component was poor on the covid resurgence and the bounce was mediocre in this report with 74K jobs added. Last month there were 42K job losses in food services and drinking places and that hasn't rebounded with few jobs added. The number of jobs in leisure and hospitality is down by 1.6m relative to Feb 2020.

Powell said this report need to be 'reasonably good' to taper in November. Is this good enough? Probably but it could slow the pace to something like $15B from $20B. That will be the next big debate.