- Prior was 3.1%

- CPI m/m -0.3% vs -0.3% expected

Core measures

- CPI Bank of Canada core y/y 2.6% vs 2.8% last month

- CPI Bank of Canada core m/m -0.5% versus +0.1% last month

- Core CPI MoM SA +0.1% vs +0.3% last month

- Trim 3.7% versus 3.5% last month

- Median 3.6% versus 3.4% has month. Revised to 3.6%

- Common 3.9% versus 3.9% last month

This is a big input ahead of the January 24 Bank of Canada meeting. The market was pricing in a 23% chance of a cut before the data and has fallen to 19% afterwards. March is down to 30% from 46%. The Canadian dollar bumped higher after the data because of a very soft Empire Fed survey released at the same time, which is weighing on the US dollar broadly.

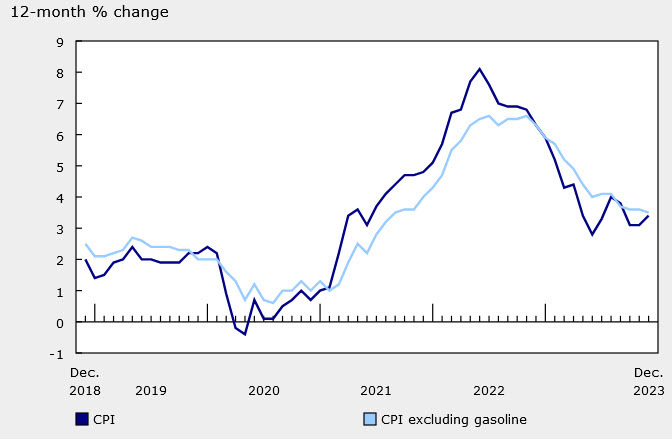

The rise in the headline to 3.4% from 3.1% comes as a -0.6% from a year earlier rolled off. However the core y/y reading fell to 2.6% from 2.8%, which is basically on target. Next month, a high headline number rolls off but core is low so we will start to see some convergence. However from the February data onwards, there will be some real help in getting these numbers to a level where the BOC is comfortable in cutting rates.

In terms of details, upward pressure came from airfares (+31.1%), fuel oil, passenger vehicles (+2.3% y/y) and rent (+7.7%). Prices for food purchased from stores rose 4.7% y/y in December. Moderating the acceleration in the all-items CPI were lower prices for travel tours.(-18.2%) and gasoline (-4.4%).