Headline measures:

- Prior y/y 3.5%

- CPI m/m +0.3% versus +0.4% expected

- Prior m/m 0.4%

- Unrounded +0.313% vs +0.359% m/m prior (consensus unrounded +0.37%)

Core measures:

- Core CPI m/m +0.3% versus +0.3% expected. Prior month 0.4%

- Unrounded core +0.290% vs +0.359% prior (consensus unrounded 0.30%)

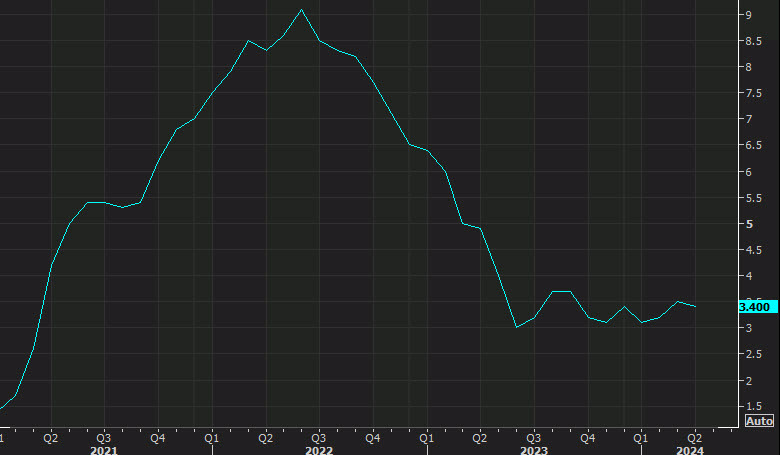

- Core CPI y/y +3.6% versus 3.6% expected. Prior month was 3.8%

- Shelter +0.4% versus +0.4% prior month

- Shelter y/y +5.5% vs +5.7% prior

- Services less rent of shelter +0.2% m/m vs +0.65% prior

- Services less rent of shelter % y/y vs +4.8% prior

- Real weekly earnings -0.4% vs +0.3% prior

- Food 0.0% m/m vs +0.1% m/m prior

- Food +2.2% y/y vs +2.2% y/y prior

- Energy +1.1% m/m vs +1.1% m/m prior

- Energy +2.6% vs +2.1% y/y prior

- Rents +0.4% m/m vs +0.4% prior

- Owner's equivalent rent +0.4% vs +0.4% prior

- Full report

Ahead of the report, the market was pricing in 47 basis points in Fed rate cuts and USD/JPY was trading at 155.59 with EUR/USD at 1.0830 and S&P 50 futures up 1 point.

After the report, the market is pricing in 50 bps in rate cuts this year and USD/JPY is trading at 155.26 with EUR/USD at 1.0854.

This is a good reading. It's not going to give the Fed confidence to cut rates but it will dull talk of further rate hikes and problematic inflation. Combine it with today's weak retail sales data and there's a developing picture of a softening economy.

One area that remained high was rents and owners'-equivalent rent. That may give the Fed some comfort because market-based numbers on those have come down, so it's more of a timing issue. Given that, they will feel comfortable that there is some disinflation in the pipeline in a component that makes up one-third of the CPI. In addition, the rises in energy prices in April have been unwound in May.

All, in gasoline and shelter were 70% of the CPI increase and that won't last.