- The final September reading was 50.1

- Manufacturing 50.0 vs 49.5 expected (prior 49.8)

- Composite index 51.0 vs 50.2 prior

- Service sector new business fell for a third month running, albeit at a softer pace than seen in September

- Manufacturers registered the fastest rise in new orders in just over a year

Another day, another data point showing surprising strength in the US economy.

Commenting on the data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“Hopes of a soft landing for the US economy will be encouraged by the improved situation seen in October. The S&P Global PMI survey has been among the most downbeat economic indicators in recent months, so the upturn in US output growth signalled at the start of the fourth quarter is good news. Future output expectations have also turned up despite rising geopolitical concerns and domestic political tensions, climbing to the joint- highest for nearly one-and-a-half years.

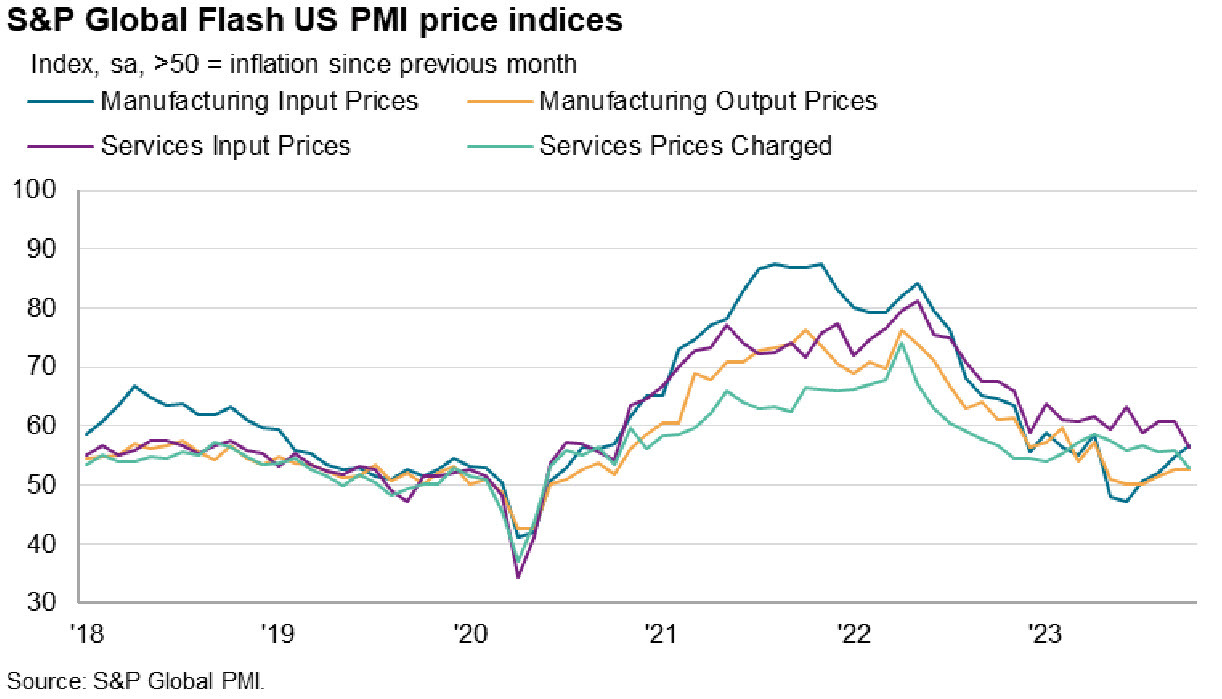

“Sentiment has improved in part due to hopes of interest rates having peaked, something which looks increasingly likely given the further cooling of inflationary pressures witnessed in October. In spite of higher oil prices, firms’ input cost inflation fell sharply to the lowest since October 2020, and average selling prices for goods and services posted the smallest monthly rise since June 2020.

“The survey’s selling price gauge is now close to its pre- pandemic long-run average and consistent with headline inflation dropping close to the Fed’s 2% target in the coming months, something which looks likely to be achieved without output falling into contraction. That said, the tensions in the Middle East pose downside risks to growth and upside risks to inflation, adding fresh uncertainty to the outlook."

Note the dip in services input inflation here; that's an area the Fed is watching closely.