-The Fed is likely to tactically delay normalization at the March FOMC meeting, with three 2016 hikes in the updated dot plot.--The FOMC should continue evaluating global risks, whereas a more "balanced" assessment would lift front-end rates.---We expect a USD-positive Fed tone, but a choppy path higher until the dollar recorrelates with rates and fundamentals.FX: a low-key Fed for a battered market. For

a market whipsawed by central bank meetings, including the ECB and BoJ,

the FX market is probably just fine with a low-volatility Fed meeting

next week. And that's what we expect from an FX market standpoint with

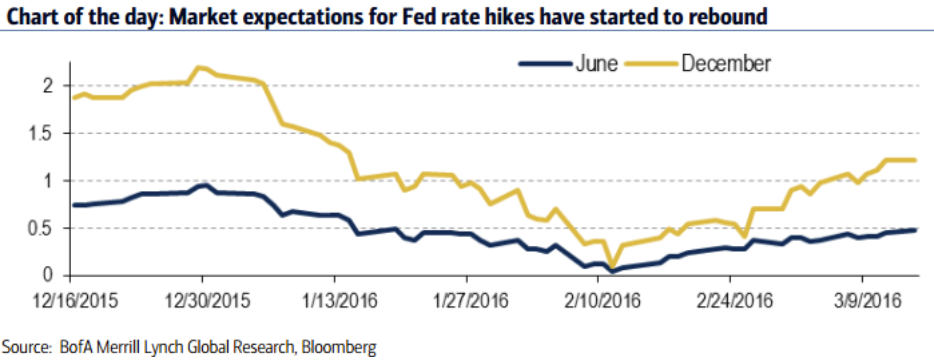

the market pricing only a small, 10% probability of a hike. More

important for the FX reaction will be the Fed's overall tone, and

assessment of the balance of risks. Since the January FOMC meeting

things are looking better on this front.

The trade-weighted USD has fallen over 3%, equities have risen over

4% and oil is up more recently. US data momentum has also improved,

reducing recession fears. In addition, ECB easing and stability in

USD/CNY have also calmed markets. So, the cautiously optimistic, data

dependent tone that we expect where the FOMC leaves its assessment of

risks as balanced will be USD-supportive. However, with the market questioning the efficacy of BoJ and ECB policy easing, we

are hesitant to establish an outright bullish USD position here, at

least until the commodity rally stabilizes or reverses and the dollar's

declining sensitivity to fundamentals reverses. We still see a steady

theme of policy divergence as USD-positive, but are cognizant the path

will be choppy and pace slow given the Fed's increased sensitivity to

USD strength. So, in some sense, the ECB's inability to weaken

the EUR, while at the same time loosening financial conditions, makes it

easier for the Fed to carry on with its gradual normalization.