Economic growth for Australia in the March quarter of 2017

+0.3% q/q ... in line with expectations but a pretty terrible result nonetheless. Growth is at its lowest in 8 years

- expected +0.3%, prior +1.1% q/q

+1.7% y/y

- expected +1.6%, prior +2.4% y/y

- Deflator +2.2% (deflator is an inflation indicator)

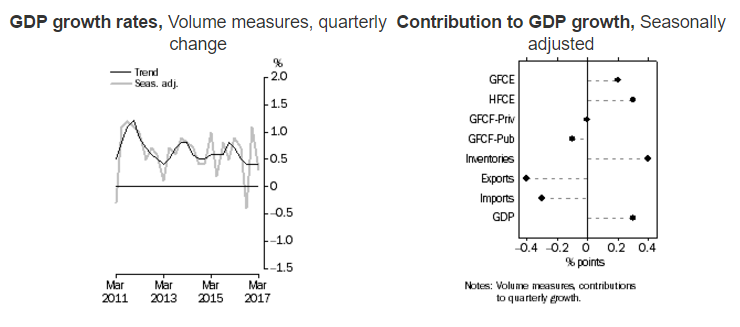

- Final consumption +0.6 of a point

- Gross fixed capital expenditure -0.6 point

That 'final consumption' is an upside surprise, especially given the run of poor retail sales data points. Capex falls, unsurprising but going foreword that is a bad sign.

More:

Exports of goods and services fell 1.6% after six consecutive quarters of growth

- A big subtraction from growth

- Exports of goods and services was the largest detractor from GDP growth this quarter, detracting 0.4 percentage points.

Dwelling investment fell 4.4% in the March quarter

- Fell 2.5% on the year

- Still at a high level nonetheless

Compensation of employees rose by 1.0% this quarter.

- Hours worked in all jobs increased 0.3%

- The March quarter 2017 Wage Price Index showed through the year growth of 1.9%

Household final consumption expenditure (HFCE) increased 0.5% in the March quarter

- Main drivers of HFCE growth were electricity, gas and other fuel (2.9%), operation of vehicles (1.3%) and insurance and other financial services (0.7%)

- Alcoholic beverages (-1.0%) and clothing and footwear (-0.7%) were the strongest detractors from HFCE growth during the quarter

- Through the year, HFCE growth (2.3%) was slightly below its long term average.

The household saving ratio is 4.7 for the March quarter 2017, down from the 5.1 recorded last quarter

- This was driven by subdued growth in gross disposable income being offset by the growth in current price household final consumption expenditure of 0.9%.

- This is the fourth consecutive quarter where the saving ratio has decreased

Terms of trade increased 6.6% in the March quarter 2017

- following a rise of 9.6% last quarter

- Driven by a 9.4% increase in the export price index.

Total inventories increased by $2,069m in the March quarter following a build up of $208m in the December quarter

- Inventories in Mining increased by $997m in the March quarter following a large run down the previous quarter

--

The 'Household final consumption expenditure' is always a wild card and it has saved the bacon this time. A lot of the other GDP components can be sussed out more or less from partial releases in the days ahead of the GDP, but not the HFCE; for that we more or less rely on retail sales data. This time HFCE has come in way higher than what retail sales indicated was likely.

Oh, and something to be alert for. I have already seen 'analysis' attributing the positive GDP result to a 'run down' in household savings. I know some readers of ForexLive also subscribe to some of the alarmist doom and gloom 'newsletters' that charge $$$ for shoddy analysis, so just be aware savings were not run down, saving actually increased, just at a slower rate. The data today is bad enough (IMO) without getting the basics wrong.

The point about a slower savings rate relates to slow wage growth, too slow. The savings rate will pick up if wage growth picks up.

Not

holding

my

breath.

At 0.3% q/q and 1.7% y/y there is still time to get long barf bags. What a bad result. Still, its better than lower than 0.3 & 1.7, right?