Goldman Sachs reviews and updates its core beliefs about the foreign exchange market this year

In late January, Goldman Sachs analysts published 10 Commandments for the 2016 FX market. Now they take a second look.

From Goldman Sachs:

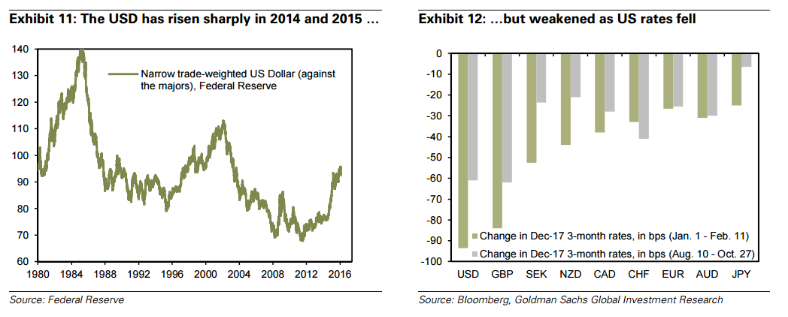

Over the past month the market has put the USD under substantial pressure, and the DXY has fallen almost 4% since the end of January. The market has all but eliminated Fed rate hikes from the US curve for the rest of 2016, and the USD is lower versus both the EUR and the JPY as risk sentiment has suffered. This sell-off has stopped us out of our 2016 Top Trade recommendation to be long USD vs EUR and JPY.

In response to this uncertainty, last month we published a list of core 'truths', which we think will prevail and dictate market direction this year. We revisit and update these below following the BoJ's January easing, and even more market turmoil in recent weeks.

1. Much more US outperformance than priced. Behind all the short-term worries lurks one important fact that is often overlooked. The Dollar has appreciated 26% versus the majors over the last two years, but US growth has stayed above trend. There is little doubt that net exports and inflation have suffered, but the resilience of the economy suggests that underlying momentum on both the growth and inflation fronts is better than priced, especially now that front-end interest rates have priced out so much tightening.

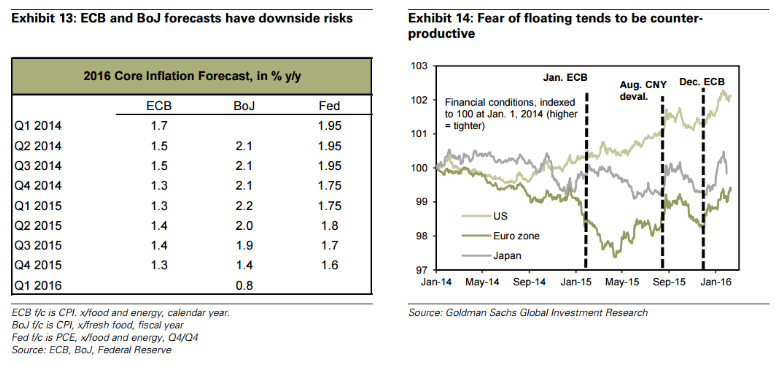

2. The ECB and BoJ can and will ease more. In the wake of recent disappointments, markets worry that the ECB and BoJ are reneging on their commitments to boost inflation, which has been weighing on risk. Both central banks have progressively cut their 2016 core CPI forecasts, fanning fears that they are 'terming out' their inflation targets. Indeed, our European Economics team forecasts core HICP at 1.0% this year, below the 1.3% ECB forecast, an illustration of the downside risk to an already low number. In our view, the January BoJ meeting demonstrated the BoJ's ongoing commitment to its inflation target, even as the market has come to doubt the efficacy of its move to negative rates. For both the ECB and BoJ, we expect more stimulus - in addition to their recent easing steps - as opposed to reneging, which is the basis for our 12-month view of $/JPY at 130 and EUR/$ at 0.95.

3. G-3 central banks will get over their fear of floating. Fear of floating among the G-3 central banks has a price, which is that it destabilises risk, inadvertently tightening financial conditions. One example is the September FOMC, which exacerbated market anxiety over China with its focus on financial conditions. Another is the December ECB, where concern over excessive Euro weakening was reportedly one driver for not taking more aggressive action. Both times, equity market declines caused financial conditions to tighten, making efforts to manage G-3 exchange rates counterproductive. We expect the G-3 central banks to accept more Dollar strength as the lesser of two evils.

4. Low inflation for longer in the Euro area. Much of the discussion over low inflation in the Euro area revolves around global themes, including falling commodity prices and the slowdown in EM. But ongoing structural reforms in periphery countries mean that price and wage levels are likely to keep falling, imparting a deflationary bias to the region, which is distinct from global developments.

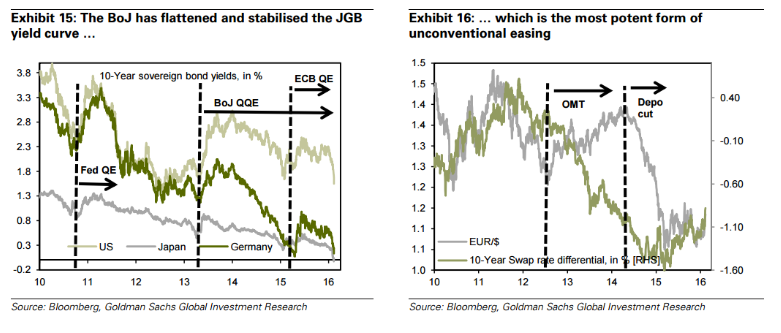

5. Negative interest rates are not a QE substitute. We estimate that a 10bp (surprise) deposit cut is worth two big figures in EUR/$, based on intra-day moves when surprise deposit cuts were announced (September 4, 2014 and October 22, 2015). This means that the bulk of the decline in EUR/$ stems from ECB balance sheet expansion and long-term interest differentials not front-end rates. Our forecast for EUR/$ down anticipates a shift in emphasis back to asset purchases from depo cuts. In the case of Japan, negative rates have augmented rather than substituted for existing QQE measures, and the impact has been to push JGB yields much lower. While the sell-off in risk assets has flattered JPY through interest rate differentials, we expect that ultimately this fall in the JGB curve will push JPY lower via portfolio rebalancing, as in point 6 below.

6. The BoJ is the ultimate QE warrior. Quantitative easing aims to boost growth via a portfolio shift out of safe-haven assets into risk assets. The QQE program has aggressively flattened and stabilised the JGB yield curve, encouraging that shift, such that $/JPY sees 'autonomous' moves up when risk appetite is good, for example in the summer of 2014 (the move from 102 to 109) and May 2015 (the move from 120 to 125). EUR/$ has not benefited from similar portfolio shifts because Bunds - the safe-haven asset in the Euro are - have been too volatile. And, as above, in Japan negative rates have not been introduced as a substitute for further QE, but as an augmentation.

7. The Dollar is a 'risk-on' safe-haven currency. The correlation of the Dollar with risk has flipped from negative to positive in recent years. This switch reflects rate differentials, rather than a loss of safe-haven status. Negative growth shocks, real or perceived, cause markets to price out monetary tightening in the US, such that rate differentials move against the Dollar. The positive correlation of USD with risk is therefore really a reflection of US cyclical outperformance.

8. Near-term pain, long-term gain for USD from low oil. Falling oil prices have a negative fall-out on economic activity in the short run, weighing on the Dollar by way of rate differentials. But the US remains a net oil importer, so that low for long in oil prices is fundamentally a Dollar positive, once near-term effects drop out. By way of illustration, it was the oil super cycle that derailed the Dollar-positive impulse from rising rate differentials in 2004-08.

9. China's balance of payments is under control. There is a lot of anxiety that the pickup in capital outflows represents a run on the RMB, making a large devaluation all but inevitable. However, a key reason that outflows were so large in 2015 was that August and December saw the RMB fix weaker, which caused (heavily expectation-based) outflows to pick up. With a current account surplus of perhaps as much as US$400bn this year, China's balance of payments can absorb a sizeable level of outflows before reserve drawdowns become necessary.

10. It is not in China's interest to destabilise the world. China is a net exporter, i.e., it depends more than other countries on sound global growth. It is therefore hardly in China's interest to unsettle markets and derail the world economy. Recent developments most likely point to a greater desire to see flexibility in the exchange rate and a closer link to fundamentals (which includes a shift in focus to a tradeweighted exchange rate), rather than unilateral devaluation.

For trade ideas from banks, check out eFX Plus.