It's tempting to read today's price action in FX as a reflection of the thinning of a crowded trade in US dollars. Yes, bond yields are lower by 2 bps but that's hardly a decisive catalyst.

Oil is more convincing as another $2 decline combined with narrowed gasoline cracks will reverse a significant area of angst about inflation and further Fed hikes. Along those lines, the market is now pricing in 76 bps in cuts next year, up from 59 bps before ADP employment.

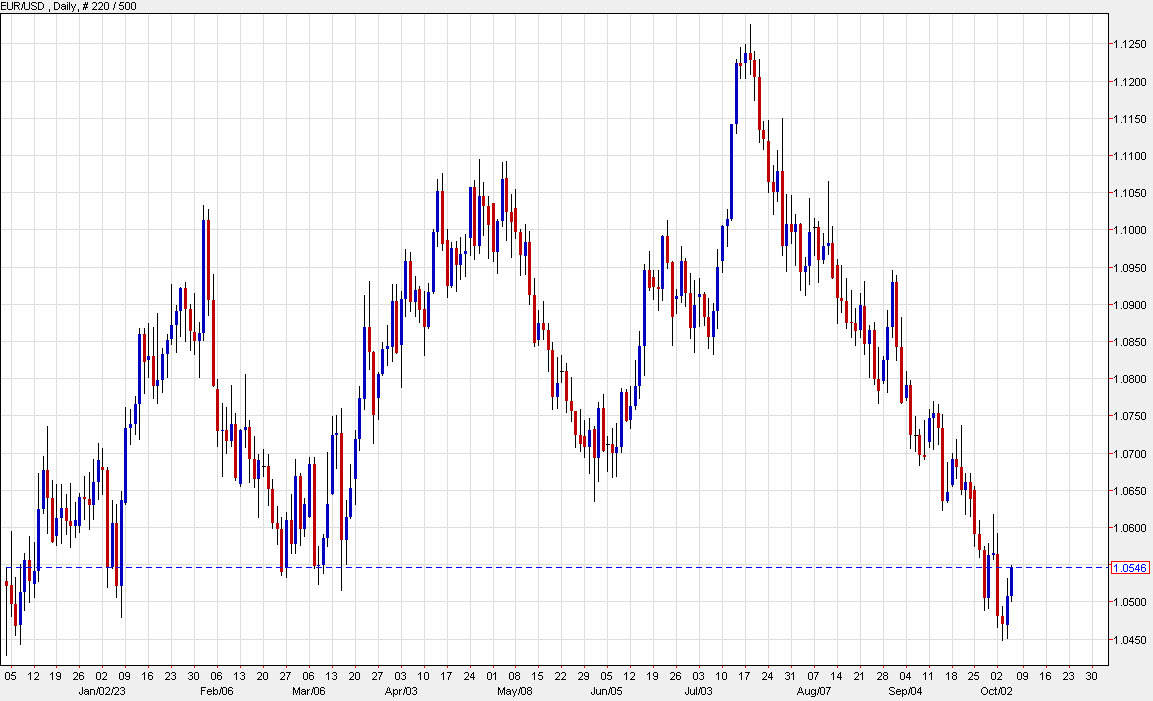

In any case, these are small (but growing) retracements after a month-long march higher in the bid dollar.

It probably won't take much of a miss in non-farm payrolls to spark a stronger rebound in the euro but there isn't much low-hanging fruit despite the look of that chart. There's just a 22 bps chance of a hike in November priced in; taking that down to zero might get the euro to 1.0600 but not much higher.