From Barclays Capital weekly FX client note, views on USD, JPY and EUR. This via eFX

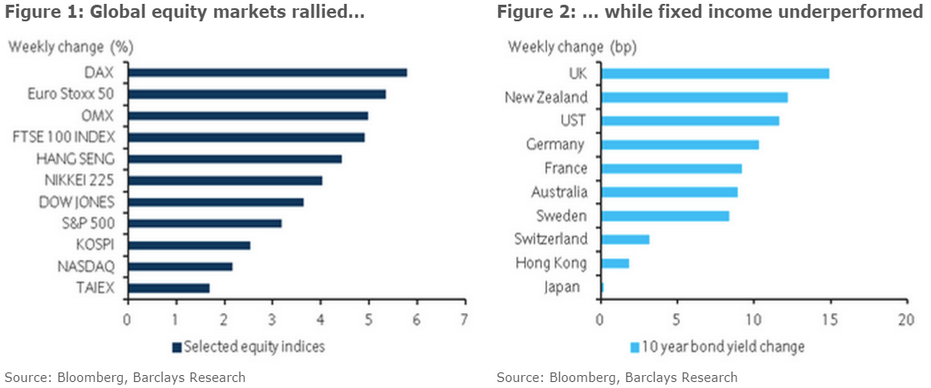

"Last week saw a significant improvement in global risk sentiment,

benefitting risky assets, despite soft data prints and cautious central

bank rhetoric (Figures 1 and 2). However, we think the market is likely heading into an environment of lower growth, soft inflation and additional policy stimulus.

Central bank rhetoric is starting to reflect this new reality. The

September FOMC minutes showed that the decision not to hike was not a

close call, though some FOMC participants had described it as such.. At

the same time, the ECB highlighted downside risks to euro area growth

and inflation while the BoE also erred on the side of caution," Barclays

argues.

In such a lower growth/soft inflation environment, Barclays

continues to see value in owning the USD due to the currency's superior

returns to capital and safe-haven characteristics.

"A China-led EM slowdown remains a real risk for markets, and we

continue to think that the relative closeness of the US economy

partially insulates it.

As a result, we think the USD's recent underperformance, partly

reflecting softer economic data and a cautious Fed, and partly

positioning adjustments, will likely prove temporary. Instead,

we continue to argue that the recent tightening of monetary and

financial conditions in countries in need of further stimulus pose clear

challenges for their growth and inflation outlooks," Barclays adds.

As a result, Barclays continues to expect further policy stimulus by many central banks.

"We look for the ECB to announce further easing before year-end

and have frontloaded our call for additional BoJ easing at its 30

October meeting," Barclays projects.

"Strategically, we like being long USD heading into those central bank meetings," Barclays advises.

In line with this view, Barclays maintains a short EUR/USD position in its portfolio from 1.1278, with a stop at 1.1562, and a targets at 1.0460.