The FOMC is finishing up their two day meeting and will grace us with their statement and press conference comments. Most traders are focused on the wording. However, they will also provide the Fed members projections for rates at the end of 2014, 2015, 2016 and Longer Term, and their “guesstimates” for GDP, Unemployment and PCE inflation. Any changing trends of member sentiment will be eyed for monetary policy clues and could provide the window into the Fed’s true bias.

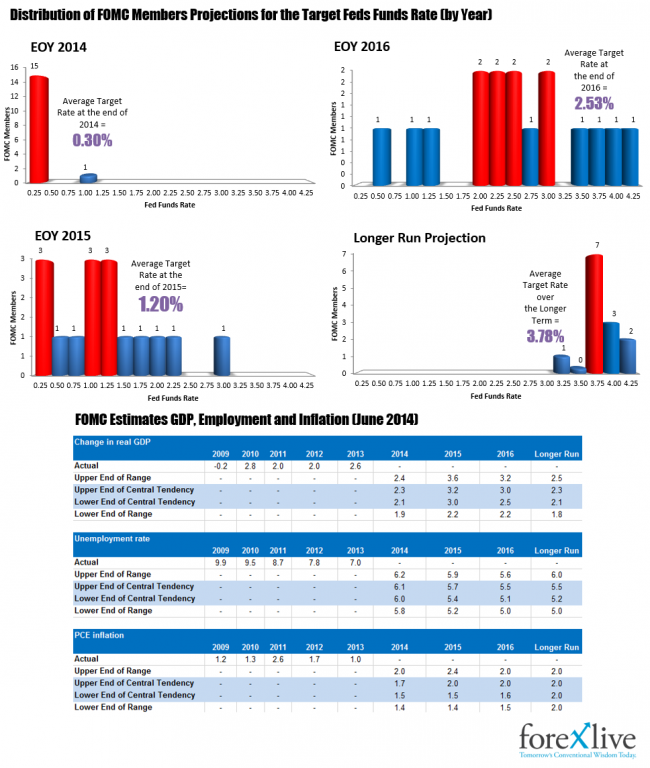

The below infograph, shows the distribution of the rate projections from the June meeting along with the growth, employment and inflation estimates.

Regarding the rate distribution, some notes:

- There was one member who thought 1% was appropriate for the target rate at the end of 2014. HMMMM, There is always one wise guy in the bunch.

- In 2015, there were 3 members who saw no change in rates in 2015 at all (I guess there may be 3 wise guys in the bunch). There was another member who thought 3% was likely. The average of the respondents see 1.2% by the end of 2015. About right? Too high? Too low? Where do you fit in with the Fed members? I am at 1% is right (3 moves). I would think the three at no change might be inclined to up their guesstimate higher. Agree?

- For 2016, four of 16 see rates reaching the “new normal” for rates (i.e., >3.5% but <4.25%). The Fed stated that the peak in rates will be lower than in the past as the damage done will act as a deterrent in the future. There are simply more controls/regulations in place that should limit sharp increases in the velocity of money and leverage excesses. I don’t think anyone wants to revisit 2008 again.

- For the Longer Run, the committee outlines the “new normal” for rates. That centers +-3.75%.

The Distibution of Rate Projections and Economic Guesstimates from the Fed Members after the June 2014 meeting.

Regarding the economic estimates, we have had one bad annualized GDP rate of -2.1% and one stronger at 4.2%. The OECD recently lowered the US GDP to 2.1% from 2.6%. When you start to go out into 2015 and 2016, economists have a tough enough time estimating the GDP in the next quarter. I don’t know if the Fed is any better. Of course the market may gauge hawkish or dovish FOMC by whether they lower or raise estimates. That will be the most important takeaway in my opinion.

Employment target shows around 6% for 2014 and 5.4%-5.7%. If 5.5% is “close to full employment” this would support rates rising in 2015 sometime.

Finally, inflation expectations are on the lower side of 2.0%. Is the Fed more worried about inflation or deflation? I don’t expect any change in commitment, but…. you never know.

The most important takeaway?

I believe, the average or median for rate projections for 2015 will be the one piece of info that the market will focus on the most. In June the average was 1.20%. The median was close by at 1.13%. The change might just be a catalyst for dollar higher or dollar lower (outside the wording of course). Be aware. Be prepared.