Back in April 2021, Goldman Sachs wrote what was perhaps the most-widely shared research note in base metals ever, titled 'Copper is the New Oil' (read it here) and it laid out supply-demand forecasts that left record deficits starting in 2026. The report also laid out a scenario for mitigating those deficits -- namely the sanctioning of new mines.

Since then two things have happened:

1) The mines haven't been sanctioned because copper prices have retraced and inflation/interest rates are making it tough to raise money

2) Governments have increased infrastructure/green spending, like the US program that will kick off next year and China building more solar

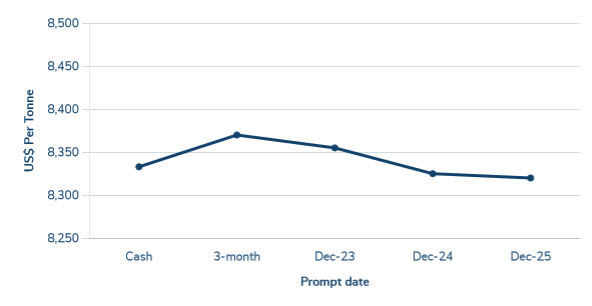

Now Goldman Sachs is even more bullish and this week delivered a 12-month forecast for $11,000/tone, up from $9000; in 2024 they see prices averaging $12,000 from $8355 currently.

Operations in Chile are undershooting production targets and that means that a projected 2023-24 surplus is at risk with inventories already near record lows.

“Another deficit in the market next year will take fundamental conditions to an unprecedented extreme in terms of tightness,” wrote GS analyst Nick Snowdon. “The sequential increase in policy targets and commitments to green transition, alongside a minimal supply response so far... have resulted in earlier and larger open-ended deficit conditions that essentially are already here, not beginning at some point in the future.”

Earlier this week, Glencore CEO Gary Nagle also predicted a 'huge deficit' and said his company wouldn't invest in adding production until the market was 'screaming for it'.