From eFX comes Deutsche Bank's comment aon the Bank of Japan and negative interest rates

The most important takeaway from last week's BoJ announcement is that there is effectively no lower bound to global policy rates - central banks can cut rates much, much more if they desire to do so, notes Deutsche Bank.

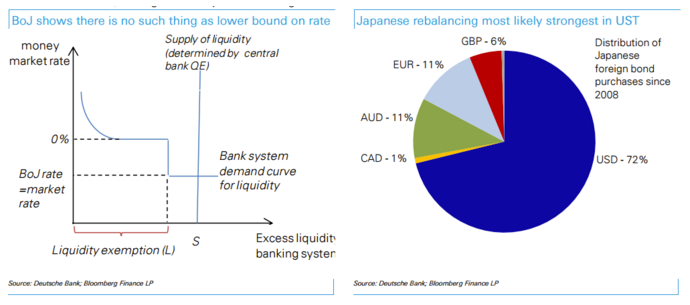

"The conclusion does not stem from the current level of BoJ rates itself; we are only at -10bps. Instead, it is the design of the system that matters. By creating dynamic and highly flexible liquidity exemption thresholds, the financial system is being shielded from the cost of negative rates. Switzerland already introduced this more than a year ago. But the BoJ design affords even more flexibility as well as incorporating a mechanism that prevents banks from hoarding liquidity in banknotes. Money market and government bond yields are not determined by the size of the exemption thresholds, but by the marginal amount of excess liquidity in the system (chart 1). Provided this is charged at negative rates, rates can be pushed as deep as required.

Beyond that, the BoJ has not only demonstrated that there is no lower bound, but also signaled that negative rates are now mainstream policy. The bank was the last QE-bank to have been rejecting negative rates. With the policy toolkit now taken on board, it now joins the ECB, BoE and Fed as formally accepting negative rates as an inevitable part of the monetary policy toolkit," DB argues.

"In sum, the BoJ provides the strongest signal to date that the previously assumed zero lower bound on rates is no longer valid. Markets should now be pricing that global rates across global fixed income can sustainably and substantially trade below zero in the current (and future) easing cycles," DB concludes.

-

I would have though the Swiss and ECB decision months and months ago would have shown the non existence of a zero bound.