Forex news for New York trade on July 14, 2021:

- Fed's Powell: Monetary policy will deliver powerful support until recoveries complete

- Powell Q&A: House price rises aren't driven by irresponsible lending

- Powell: Fed lacks certainty on transitory inflation but believes it to be the case

- Bank of Canada tapers by $1 billion/week compared to $1 billion expected

- Macklem Q&A: Highlights three reasons inflation will be temporary

- BOC's Macklem: My message today is increased confidence and continued attention

- Democrats plan to fund $3.5T infrastructure with tax changes, health savings and growth

- Beige Book: US economy displayed moderate to robust growth

- BOE's Ramsden: I can envision considering tightening sooner that I previously expected

- US weekly EIA oil inventories -7897K vs -4359K expected

- Manchin says he is open to the $3.5 trillion infrastructure plan

- ECB's Schnable: We're past the turning point and seeing a strong recovery

- US PPI final demand for June 1.0% vs 0.6% estimate

- Canada May manufacturing sales -0.6% vs +1.0% expected

Markets:

- Gold up $19 to $1827

- US 10-year yields down 6.6 bps to 1.349%

- WTI crude down $2.52 to $72.73

- S&P 500 up 5 points to 4374

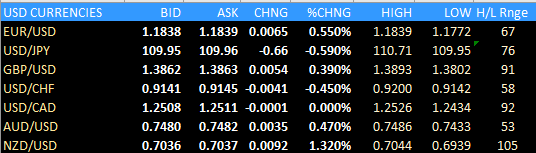

- NZD leads, USD lags

It was a packed day of news but it didn't translate into a straight-forward day of trading. No single theme or news item captured the market's imagination. Early on, Powell's words boosted the risk trade and weighed on the dollar but that faded later.

In Canadian dollar trading, the market clearly wanted more in terms of tapering or positioning the BOC for earlier rate hikes but it didn't come. Macklem stressed higher confidence in the recovery and bumped up growth forecasts but the timeline on the output gap closing stayed in H2 and the loonie fell. Sinking oil prices after looser US inventory data also didn't help.

USD/JPY was weighed down as the bond market came back to life. Yields were persistently pressured, perhaps with the Democrat's infrastructure plan to be paid for. Powell's lack of urgency on inflation was another culprit.

The antipodeans managed to hold onto earlier bids after the RBNZ taper surprise. Aside from oil, commodities were solid.

The euro staged somewhat of a recovery after yesterday's rout. That's the name of the game at the moment with few lasting trends as we sort through the summer doldrums.