UPCOMING EVENTS:

- Monday: BoJ Summary of Opinions, Swiss Retail Sales, Eurozone Unemployment Rate, US ISM Manufacturing PMI.

- Tuesday: RBA Policy Decision, Swiss CPI, US Job Openings.

- Wednesday: RBNZ Policy Decision, Eurozone Retail Sales, Eurozone PPI, US ADP, US ISM Services PMI.

- Thursday: US Challenger Job Cuts, US Jobless Claims.

- Friday: Japan Wage data, Swiss Unemployment Rate, US NFP, Canada Jobs report.

Monday

The Eurozone Unemployment Rate is expected to remain unchanged at 6.4%. The labour market remains tight and central banks would like to see it softening to have more confidence on a timely and sustainable achievement of their inflation targets.

The US ISM Manufacturing PMI is expected to tick higher to 47.7 vs. 47.6 prior. As a reminder, the S&P Global US Manufacturing PMI beat expectations, although it remains in contraction, and overall the comments point to stagnation in activity.

Tuesday

The RBA is expected to keep the cash rate unchanged at 4.10%. The RBA expected headline inflation to pick up in Q3 due to higher energy prices and highlighted that the labour market could be at a turning point. Indeed, the latest labour market report was lacklustre as the bulk of jobs added were part time and the latest monthly CPI showed a pick up in headline inflation with the Core measure decreasing.

The US Job Openings will be one of the top releases this week as the big miss in the previous month caused some notable moves in the markets due to the focus on the labour market data. The consensus sees Job Openings to remain basically unchanged for August at 8.83M vs. 8.827M for July.

Wednesday

The RBNZ is expected to keep the Official Cash Rate unchanged at 5.50%. The central bank is confident that with the current level of interest rates inflation will return to target and it’s ready to look through some strength in the data in the near term as communicated in the latest policy statement.

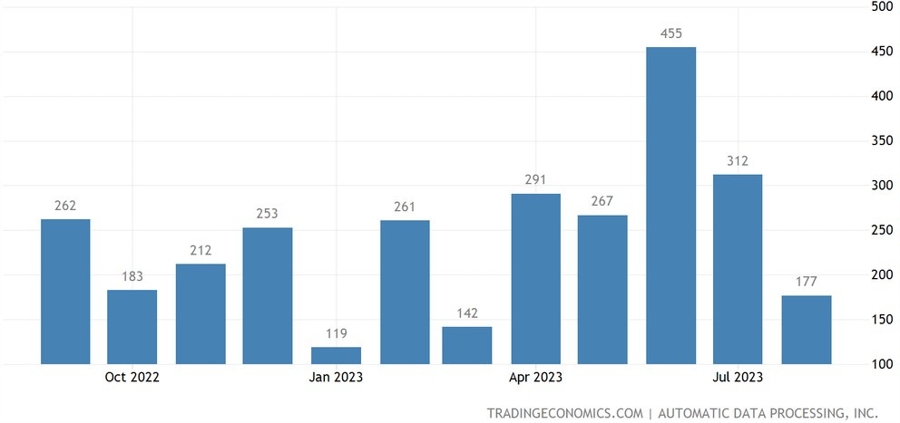

The US ADP is a labour market report and as such it has the potential to move the markets. The consensus sees 160K jobs added in September compared to 177K prior.

The US ISM Services PMI is expected to tick lower to 53.6 vs. 54.5 prior. The latest S&P Global US Services PMI missed expectations, although the index remained in expansion. Again, the comments pointed to contracting demand and waning activity.

Thursday

The US Jobless Claims data continues to be one of the top releases each week as the focus has now turned more towards the labour market. Last week, the data beat expectations again in a sign that the labour market remains solid for now. There’s no consensus at the moment, but keep an eye on it as it remains a key labour market report.

Friday

The Japanese wage data is going to be important for the BoJ as the central bank continues to repeat that it wants to see a solid growth in wages to be confident on a sustainable achievement of their inflation target and the consequent exit from monetary easing. Notably, the data has been trending lower in the past few months.

The US NFP is expected to show 163K jobs added in September compared to 187K seen in August and the Unemployment Rate to tick lower to 3.7% vs. 3.8% in the prior month. The Average Hourly Earnings will also be a key metric to watch with the yearly growth seen at 4.3% vs. 4.3% prior and the monthly one at 0.3% vs. 0.2% prior. Also, watch out for the revisions as the prior months continue to be revised downwards.