- Think of US inflation reports like a golf scorecard

- French central bank boosts 2022 GDP forecast but cuts 2023

- Tropical storm Fiona won't be a risk to energy markets

- World Bank: Core inflation excluding energy could be 5% in 2023

- Atlanta Fed GDPNow cut to 0.5% from 1.3% previously

- European equity close: French equities lead the downside in third day of losses

- Gold hits stops on a major technical break

- Ethereum takes a 5% dive as the sell-the-fact trade hits

- US July business inventories +0.6% vs +0.6% expected

- The morning forex technical report for September 15, 2022

- US August industrial production -0.2% vs +0.1% expected

- Canadian August home price index -1.6% m/m

- Why the US dollar is sliding after today's heavy data slate

- US initial jobless claims 213K vs. 226K estimate

- US August import price index -1.0% m/m vs -1.2% expected

- US Sept Philly Fed business index -9.9 vs +2.8 expected

- US Empire manufacturing index -1.5 vs. -13.0 estimate

- US August advance retail sales +0.3% vs 0.0% expected

- Forexlive European FX news wrap 15 Sep

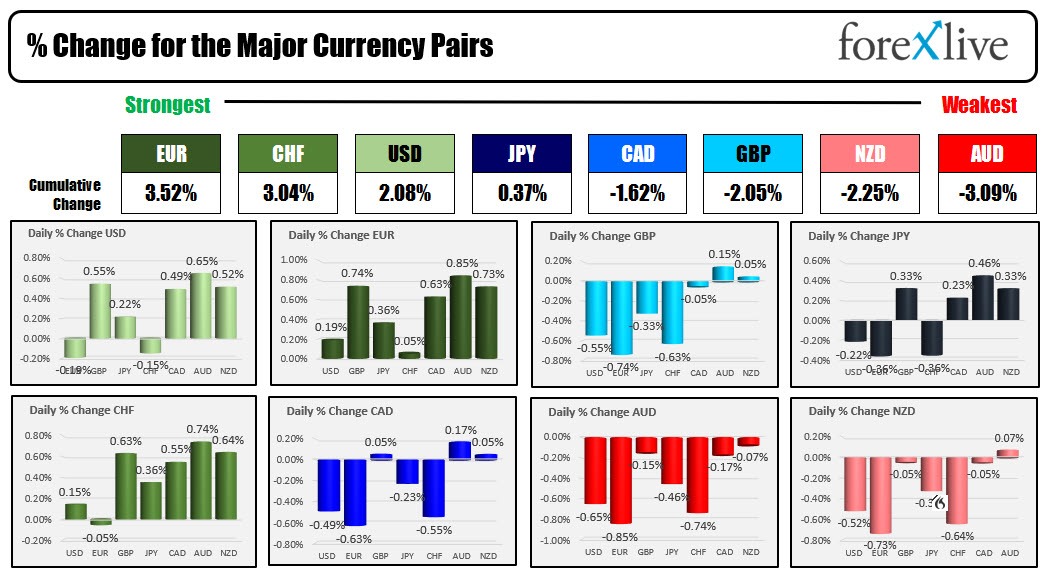

- The CHF is the strongest and the GBP is the weakest as the NA session begins

The US had a data dump today with Retail sales being the highlight. After all the dust settled with that report with the various breakdowns and revisions which were fairly impactful (headline was -0.4% from +0.0% initially reported and core revision to 0.0% from +0.4%. The control group this month came in flat vs 0.5% estimate.

Meanwhile, the weekly initial claims came in at 213K which was below the 226K estimate. That is the lowest since early June and the 5th consecutive decline (the high reached 262K).

The regional Fed indices on manufacturing canceled each other out with the Philly Fed index fell -9.9 vs +2.8, but the Empire improved markedly to -1.5 vs -13.0 estimate. For both indices, the prices paid components did fall and has moved markedly lower over the last few months, but still remains with a positive number (i.e., more businessed reporting higher prices vs lower prices). For the Philly Fed, the price paid came in at 29.8 v 43.6. For the Empire, the prices paid came in at 39.6 vs 55.5.

With the CPI still elevated, and employment still showing strength, the Fed has no choice but to stay on the path of higher rates to slow jobs and inflation even though demand seems to be slowing. It is a tough time for the fed.

The markets did not slower growth/better jobs all that well.

The US stocks moved back into the red after a "dead-cat-bounce" day yesterday. The Dow fell -0.56%. The S&P fell -1.13% and the Nasdaq fell -1.43%. All are down on the week with one day to go (PS tomorrow is quad witching hour day so be aware of the volatility possibility from that tomorrow).

IN the US debt market, yields moved higher with the 2 year up 7.1 basis points to 3.863%. The high today reached 3.877% which was another new high yield going back to 2007. For and the benchmark 10 year it is up 4.2 basis points to 3.448% after reaching 3.468%. The high for the year last month rache 3.497% which was the highest level since March 2011.

In the forex market, the EUR is ending the day as the strongest of the majors (followed by the CHF). The AUD and the NZD were the weakest.

The AUDUSD eeked out a new year low and traded to the lowest level since May 2020 at 0.66954.The pair is trading just above that at 0.6700 into the close..

The USDCAD broke above its 2022 high and traded to its highest level since November 2020 to 1.3239. Stay above 1.32054 is close risk going into the new day (low of break area between 1.3205 to 1.3222).

The GBPUSD is closing near the low for the day (at 1.1465) and is getting closer to 2022 extreme lows with 1.1442 to 1.1450 as the next support target, followed by the low for the year at 1.14042 (the March 2020 low was at 1.1408).

For the EURUSD, it is stuck between close support at 0.99515 and resistance around the 50% retracment of the move up from the September low at the 1.0030 level.

The USDJPY remained above its 100 hour MA at 143.17 and 200 hour MA at 143.04. Stay above is more bullish. Move below is more bearish in the new trading day.

Gold fell sharply on the back of higher rates. It is trading down -$32.29 and to the lowest level since April 2020.

Bitcoin is trading back below $20000 at $19814. Etherium after the Merge is down -$102 or -6.4% at $1500 after trading as low as $1459.

Crude oil is at $85, down over -$4 on the day.