- US stocks put together back-to-back up days to end week. S&P and Nasdaq close week higher

- Gold trades lower on the week

- Crude oil settles the week at $91.59 and that is lower on the week

- Dallas Fed trimmed mean PCE inflation 3.5% vs 3.1% prior

- Baker Hughes oil rig count up 2 to 522 in the current week

- Atlanta Fed GDPNow falls to 0.6% from 1.3% on Feb 17

- UK's Johnson: Urged leaders to take immediate action against SWIFT to inflict maximum pain

- NATO's Stoltenberg: Russia's aim to is to change Russian government in Kyiv

- Feds Bullard: Direct links of Ukraine/Russia is minimal

- European major indices closing higher on the day but lower on the week

- Goldman Sachs sees risk of $125 oil. Why it will be tough to bring on supply

- Kremlin says Putin has agreed to organize negotiations with Zelensky

- Final Feb UMich consumer sentiment 62.8 vs 61.7 expected

- US January pending home sales -5.7% m/m vs +1.0% expected

- ECB's Lagarde: The ECB is closely watching the situation in Ukraine

- Russia's Lavrov to visit Geneva on Monday

- Kremlin readout on Putin's call with Xi was certainly supportive

- US January core PCE +5.2% y/y vs +5.1% expected

- US January preliminary durable goods orders 1.6% versus 0.8% expected

- OPEC+ likely to stick to existing policy at March 2 meeting - report

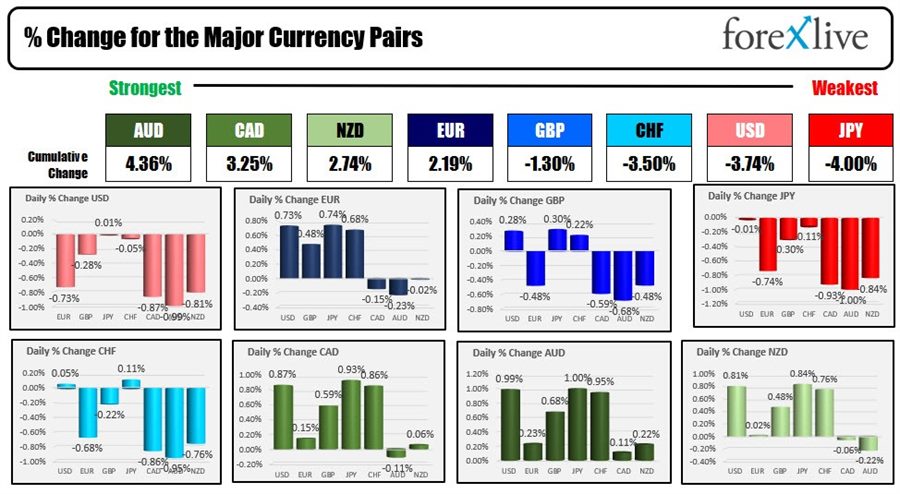

- The AUD is the strongest and the CHF is the weakest

- ForexLive European FX news wrap: Market nerves settling in as Kyiv comes under siege

The US stock indices tacked on another positive performance with the Dow taking the center stage with it's biggest day in 2022. The Dow rose 834 points on the day or 2.51%. The Nasdaq was the weakest performer but it still added 1.64% after yesterday's 3.35% gain. The S&P rose 95.95 or 2.24%. European shares also close sharply higher with gains 3.5% or more in the major indices.

For the week, the Nasdaq, S&P and Russell 2000 closed higher (by 0.8%, 1.07% and 1.58% respectively) but the Dow closed unchanged and the European shares were lower for the week.

Nevertheless, the gains today were impressive given the increased risk of a Russian takeover of Ukraine (with a new puppet government put in charge).

Now there were reports that Russia would be willing to meet with Ukraine, and perhaps that squeezed shorts and pushed underinvested to get more invested, but come next week, it may be a different story if meetings with Ukraine end with "Your choice is to step aside and let me put in new leaders". NATO may not like that idea, especially given the Russian's leader seeming desire to hold build more monopoly pieces, and Ukraine's bordering of Belarus, Poland, Slovakia, Hungary, Romania, Moldova as potential properties.

NATO nations imposed more sanctions on Russia, and the US and Europe announced sanctions on Putin freezing his personal assets.

In other news today,

- Durable goods came in better than expected with revisions to the prior month higher as well

- January core PCE came in higher at 5.2% vs 5.1% expected. Inflation remains stubbornly high keeping the hopes for 50 BP hike a possibility in March. Fed's Waller said as much last night - CLICK HERE - joining Fed's Bullard (Bullard is still calling for 100 bp by July implying one 50 BP move between now and then). The Fed Chair testifies on Capitol Hill next week and his comments will be eyed closely for clues on HIS intentions.

In the forex market, the flow of funds took it's clues from the rising stocks and a "risk on" theme. The strongest of the majors were the AUD and the NZD. The weakest were the JPY and the USD (classic risk on flows).

Some technical comments on some of the major pairs:

- The EURUSD is closing near highs at 1.1270. The pair is also testing the 100 hour MA at 1.12726 (and moving lower). The pair has nearly retraced all the declines post the Russian invasion (1.1285ish). A move back above the 100 hour MA will have traders looking toward the 1.1300 and the 200 hour MA at 1.1315

- The GBPUSD consolidated in up and down trading on Friday closing at 1.3412. The 38.2% of the move down from the Feb 18 high comes in at 1.13134. That may be a barometer for buyers and sellers next week.

- USDJPY traded down and back up on Friday. The low stalled right at the 200 hour MA at 115.14 and bounced back to and through the week high from Thursday at 115.685 to a new week high of 115.75 before settling back lower at 115.53. Watch 115.368 early next week for support. That is the 50% of the range since the Feb 10 high. Move below and we could be heading back to the 200 hour MA.

- NZDUSD moved higher today and traded above the 100 hour MA at 0.6729 currently for most of the NA session. That level will be a bias defining level at the start of the week. Stay above is more bullish. Move below and we should see further downside probing. The price is settling at 0.6745

- AUDUSD. The AUDUSD also moved back above it's 100 hour MA at 0.7205 and stayed above in the North American session on Friday. Stay above is more bullish in the new trading week.

In other markets:

- Spot gold is trading down -$14.86 or-0.78% at $1888.08. That is $86 lower than the intraday high reached yesterday and takes the price lower on the week. Last Friday, the spot gold price closed at $1898.23

- Crude oil futures are closing at $91.94 which is down $-0.87or -0.94%. Like gold, it too is well off the Thursday spike high at $100.15 and also lower on the week (last week, the contract closed at $92.00.

Soft commodities like wheat and corn took center stage this week as Russia and Ukraine are big exporters of those commodities.

- For wheat, a day after being limit up, it closed down the $0.75 daily limit today at $8.59 after trading as high as $9.60 earlier in the day (down -10.5% from the high).

- For corn futures, it followed up trading up limit during parts of yesterday at $7.189 and was down at $6.59 today (-8.39% from the high yesterday)

In the US debt market, the yields are closing off their highs of the day but mixed. For the week, the 2 year yield ticked to the highest level since December 2019 at 1.644%, but backed off to 1.57% at the close of the week. The 10 year yield a week ago closed at 1.934%. This week the low yield moved to 1.847% (on flight to safety bid), but is back up at 1.963% for a modest gain on the week. This week, the treasury auctioned off $52B of 2 year notes, $53B of 5 year notes and $50B of 7 year notes all with strong international and domestic demand. What we know is with stock markets iffy, the demand for US debt at higher rates is a good alternative.

Next week is a busy week:

- RBA rate decision on Tuesday (10:30 PM on Monday). No change is expected but market will be looking for nuances from the statement

- US ISM on Tuesday at 10 AM ET

- OPEC meeting on Wednesday. No change from the increase production expected

- ADP non farm payroll (it has been way off of late) at 8:15 AM on Wednesday

- BOC rate decision on Wednesday with expectations for a 25 bp hike

- Fed's Powell testifies at 10 AM on Wednesday and again on Thursday

- ISM service on Thursday at 10 AM ET

- US employment on Friday at 8:30 AM ET (+400K estimate).